Like a montage set to music: a big week of data for markets

Like a montage set to music: a big week of data for markets

Have you ever looked back on a busy week in your life like it’s a movie montage? Thinking of it in moments set to music? I had one of those — imagining it being set to a rock song from 1970 that my son loves and doesn’t stop playing (insert eye roll emoji). And the busyness is not over!

The highly anticipated DJ Pow will hit the decks (FOMC announcement) later today at 2pm, followed by the normal Q&A. While it’s widely expected they will announce a 0.25% increase in interest rates, bringing the Fed Funds rate to 4.75%, I’m most interested in:

The Fed’s messaging around when they will end their hiking cycle (the market expects this by spring, which I agree with right now)

Even more importantly, how they will guide how long this level of rates will stand

Right now, the market is giving a decent probability to the Fed cutting rates later in the year. My guess is the Fed will try to sway the market away from that thinking — stating they will be committed to these levels for a while. This, in turn, could bring a negative reaction as the market readjusts to higher rates than it had expected later in the year.

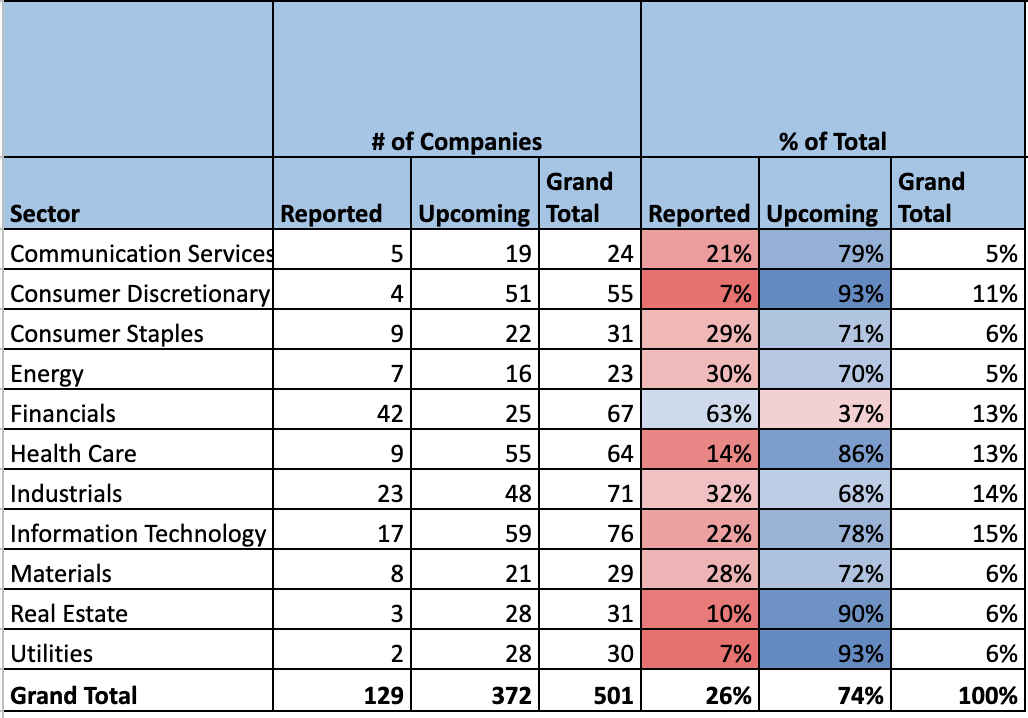

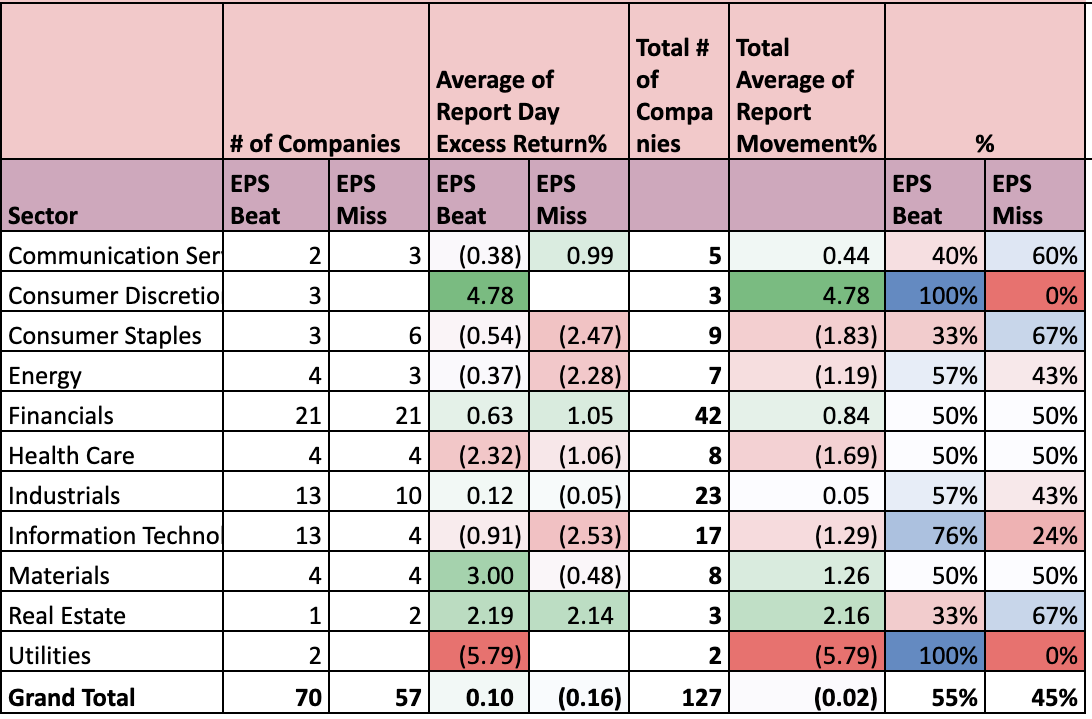

And with earnings season in full swing, Thursday, February 2 will be the biggest day of the US reporting season — bringing us earnings reports from nearly 18% of the market cap of the Russell 1000 Index (which generally represents the largest 1,000 US companies). This includes companies such as Apple, Amazon, Alphabet, Qualcomm, Ford, and Starbucks.

So far, earnings have generally been showing negative year-over-year growth rates while margins have contracted. Earnings are tracking at around a -3.8% growth rate year-over-year. While we are still seeing some companies beat expectations (~60% of those that have reported), it’s less than the last four-quarter average of 70% of companies beating expectations. See below for a snapshot of the earnings monitors we created for ourselves*:

Data as of 01/30/2023

In our 2023 outlook, we expected a less promising earnings season, BUT did not expect to see the market shrug it off, day in and day out, like it has. So there are a couple of phenomena that I am watching related to this:

Recall, all else equal, lower interest rates allow for higher stock values and vice versa. Since the start of the year, the 10-year Treasury yield has fallen from 3.9% to 3.5%. That has certainly been supportive of the rally year-to-date, contributing to said shrug-off. Will these longer term interest rates continue to fall, or rise again? Some of it depends on inflation expectations. And we won’t get the next CPI report for about two weeks, on February 14. It also depends on demand for treasuries, because typically with greater demand comes higher bond prices and lower rates (or vice versa). Demand could be there from one sizable investor — the many trillions of dollars still left in US pension plans. After many years (over a decade), their collective asset base has recovered relative to their liabilities, as assets grew in value while liability values have fallen. These plans will likely want to lock in this status by selling stocks they hold and buying bonds (to increase stability). Lower rates resulting from this could be supportive for the stock market but then again, net equity sales could offset that. Something to be aware of as things unfold.

Layoffs have been building, yet employment numbers have remained generally strong. Most of the layoff announcements came late last year and have been increasing into this month (over 70,000 employees have been laid off in January vs. over 159,000 in all of 2022). As a result, they haven’t worked their way into the data due to severance, etc. Some may have found jobs, too. But at some point, I expect it to make a mark in the data. If it does, this may have a derivative effect, as it means the Fed would really be at the end of their rate hiking cycle and — if employment weakens enough — might even consider a cut in rates. But it’s a big “if” for now.

Of course, and especially in light of earnings so far, stock market valuations overall still feel high — something that makes me feel the resistance level at 4100 on the S&P 500 will be tough to break. And we are close to it… another moment to keep in mind.

So here’s to keeping music on in the background as we grind through the news to come.

Source: Robinhood Financial, Bloomberg

*In case you noticed in the earnings monitor we shared, the number of companies that beat or missed EPS (earnings per share expectations) is 127 versus the number of companies that reported is 129. That’s because two of the companies, in healthcare and consumer discretionary, did not have any estimates prior to reporting.