What we needed from the market’s DJ (Powell) and thoughts on the other market star

What we needed from the market’s DJ (Powell) and thoughts on the other market star

On vacation recently my family and I found ourselves caught in a crowded yet small town with very little parking. Loop after loop, we drove around, as I watched the clock tick past our reservation time. Then I remembered a friend sharing her approach to this. So I closed my eyes and imagined us finding a spot from someone leaving, said please and thank you in my head, and then let it go. And wouldn’t you know, within a few minutes we found such a spot, cramped in a little alleyway, making it to dinner.

Call it magic or coincidence, but I got what I needed at that moment.

So did the market—and perhaps the economy—last Friday. The market’s DJ, Powell, and his statements at Jackson Hole all but guaranteed that the “time had come” for the Federal Reserve to begin cutting interest rates at the next meeting (September). Why? Outside of inflation now on a “sustainable path” lower, employment and any further weakening of the labor market is of equal concern as inflation.

We’ve since seen economically sensitive areas and sectors outperforming—with small caps, banks, and real estate stocks up over 3% in just the last few days, while the tech-heavy Nasdaq is down over -1%.

Why would this happen?

Since debt becomes cheaper, companies that require more debt to operate (like small caps and real estate) may be able to refinance and secure lower interest rates, which can, in turn, boost their profitability.

Second, interest rates are used as an input when valuing assets like stocks or companies. So expectations of interest rates show up in valuation metrics, such as the price-to-earnings ratio. Typically, lower rates = higher valuations and subsequently positive returns.

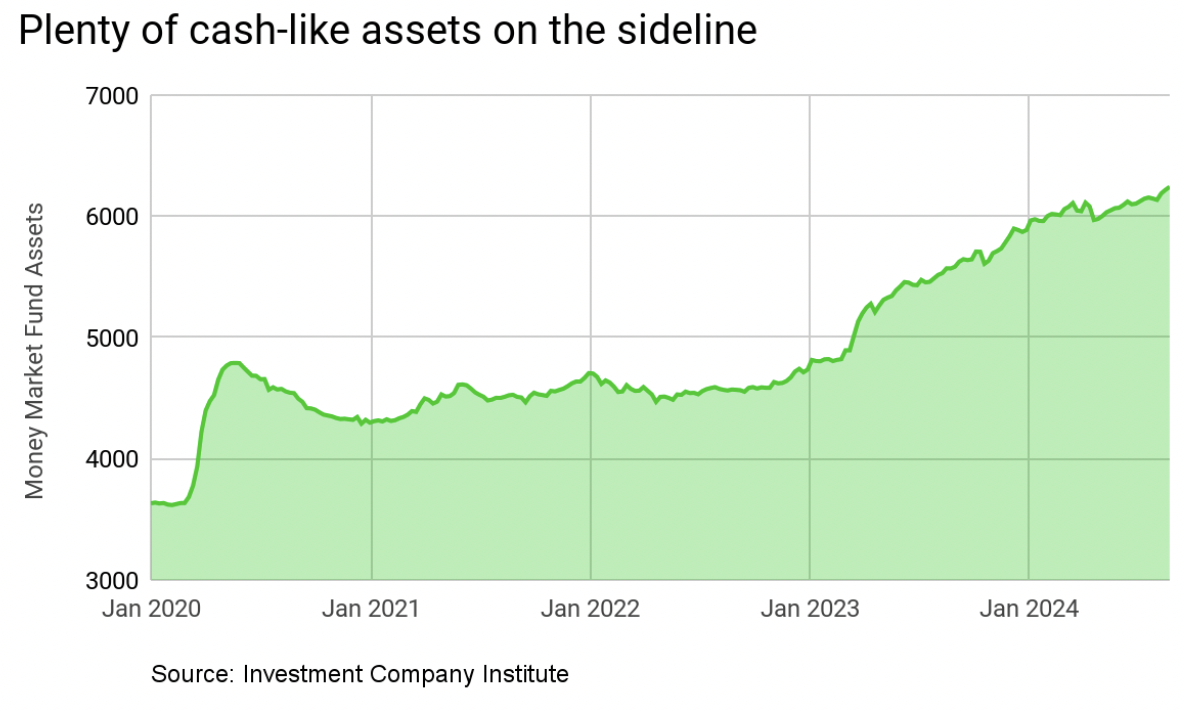

What else might happen if rates are continuously cut? With lower Fed rates, cash deposits start to earn less, so holding cash can become less attractive and many investors may eventually look for other ways to earn a return on their cash. Of course, where that goes depends on the investor's goals and timeline. For example, if you had no specific purpose for cash you held, it might eventually get invested in stocks or bonds as the deposit rate on that cash drops. There is a lot of cash potentially at play—between institutions and retail investors, roughly $6.2 trillion sits in money market funds.

What it means for us, excluding the market: The interest rate the Fed controls—the Fed Funds rate—can be thought of as the interest rates used for financing short-term debt. So it can directly affect things like credit card rates, rates on new home equity loans, and lines of credit. While there is a less direct impact on debt such as mortgages, a cut in the Fed Funds rate should mean lower financing cost for consumers.

Market expectations for a 0.50% rate cut at the September meeting have increased, with a 36% probability, up from 30% a week ago. I believe the first cut will be 0.25%, so there may be some overzealousness embedded in markets.

And speaking of potential overzealousness:

Nvidia reported earnings this afternoon. Going into it, consensus expected revenue to exceed the upper-end of the company’s guidance range for the quarter, and gross margin, which has been an important measure this earnings season, to be above the midpoint of guidance. In addition, its expected their earnings growth will be 77% next quarter and 30% over the next year. 92% of analysts have an overweight rating. In short, expectations were high and this always makes me nervous as an investor. This is because as a company gets more popular, it can beat expectations, but the amount it beats by gets smaller and smaller as the bar rises with their success. The company’s report beat consensus estimates in most areas but margins were just about in line. In addition, the focus on a potential Blackwell chip delay seems to be a “nothing burger” for now. I think you’ll see it drift lower after hours, likely dampening the tech sector tomorrow.

So there you go—we got what we needed from the Fed for now but maybe not from the most closely watched tech company.