The EV Industry: High Voltage Dreams or Low Power Reality?

The EV Industry: High Voltage Dreams or Low Power Reality?

Every time I am in northern California, I am suddenly aware of how many electric vehicles (EVs) I see. From rideshares to everyday people, they’re kind of everywhere. This stands out to me because it doesn’t feel like that here in NYC. Or any of the other cities and states I’ve traveled to.

So I checked up on my feeling and found, it’s real. According to the Alternative Fuels Data Center, the percentage of registered vehicles that are EVs is highest in California at 2.5%, while NY is at 0.75% and neighboring Connecticut and NJ are at 0.75% and 1.2%, respectively. Then I fell down a rabbit hole on the EV industry as a whole—and thought it may be worth sharing it here.

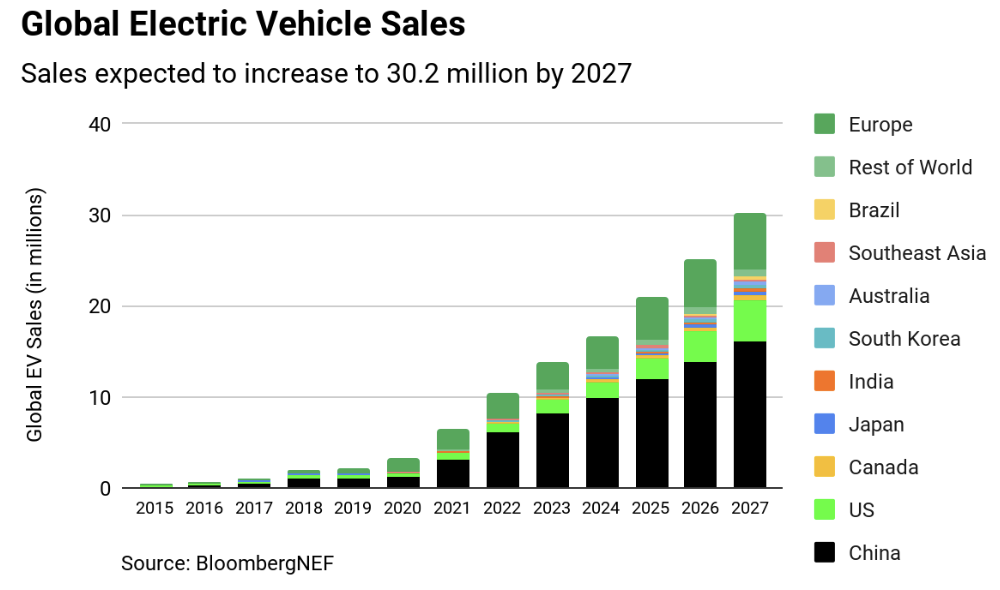

Around 2021, hype on electric vehicles started to really pick up steam. EV sales doubled as nations and select US states implemented incentives to promote net carbon goals while advances in technology made vehicles generally more affordable. Expectations might still be quite steep. For example, according to BloombergNEF, global electric vehicle sales are set to reach 30 million by 2027, well above the 14 million sold in 2023. That said, it does reflect a 21% annual growth rate, vs. the 61% growth rate between 2020 and 2023.

Despite these impressive expectations, future demand is uncertain

Consumers are wary of electric vehicles. In a study done by McKinsey, roughly 46% of current US EV owners and 29% of global EV owners indicated they would actually switch back to traditional vehicles due to issues with chargers.

Why?

Part of the issue is EV battery ranges. Since 2022, consumers have demanded 5% more range, while the actual range has only increased by 2%. And personally, that has been my biggest concern—for fear of getting stuck somewhere which feels more likely than running out of gas.

Another concern is access to chargers. The Department of Energy reported that as of February 2024, there were approx 61,000 charging stations — much lower than the estimated 145,000 gas stations in the US.

As time has gone on, there is also another hesitation—the actual cost of ownership being higher than the perceived cost.

For one, while the selling cost of electric vehicles have come down, they are still higher than their gas-guzzling counterparts. According to Edmunds, in Q1 2024, the difference between the average price of an electric vehicle compared to a gas vehicle was 42%.

Insurance costs make this disparity greater. According to the National Association of Insurance Commissioners, insuring an EV in the US can cost up to 20% more than a gas-powered car, while the cost is even higher in other countries.

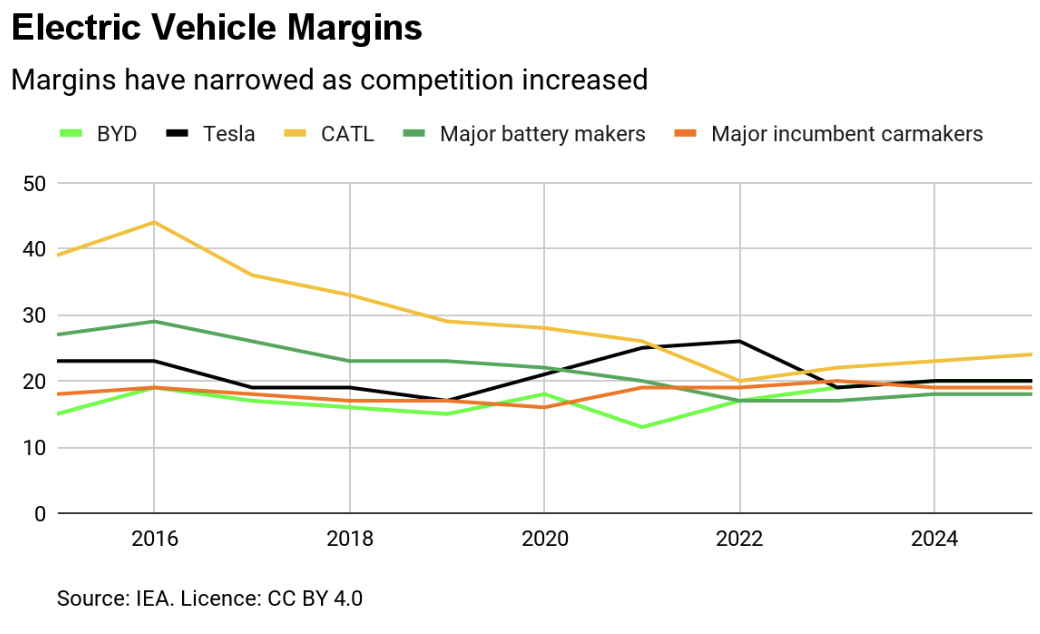

Meanwhile from an investor’s perspective, increased competition has started to shift profitability. Advances in battery technology may have initially helped early adopters enjoy robust margins. But cheaper batteries have now allowed more companies to enter the market, eroding market share and, with it, margins. According to a report by the International Energy Agency, between mid-2022 and early-2024, Tesla cut the price of its Model Y by $15 to $20k in the United States while battery costs only fell by $3k. In the US, for example, Tesla’s market share of the electric vehicle industry has shrunk from over 60% in 2020 to roughly 45% in 2023.

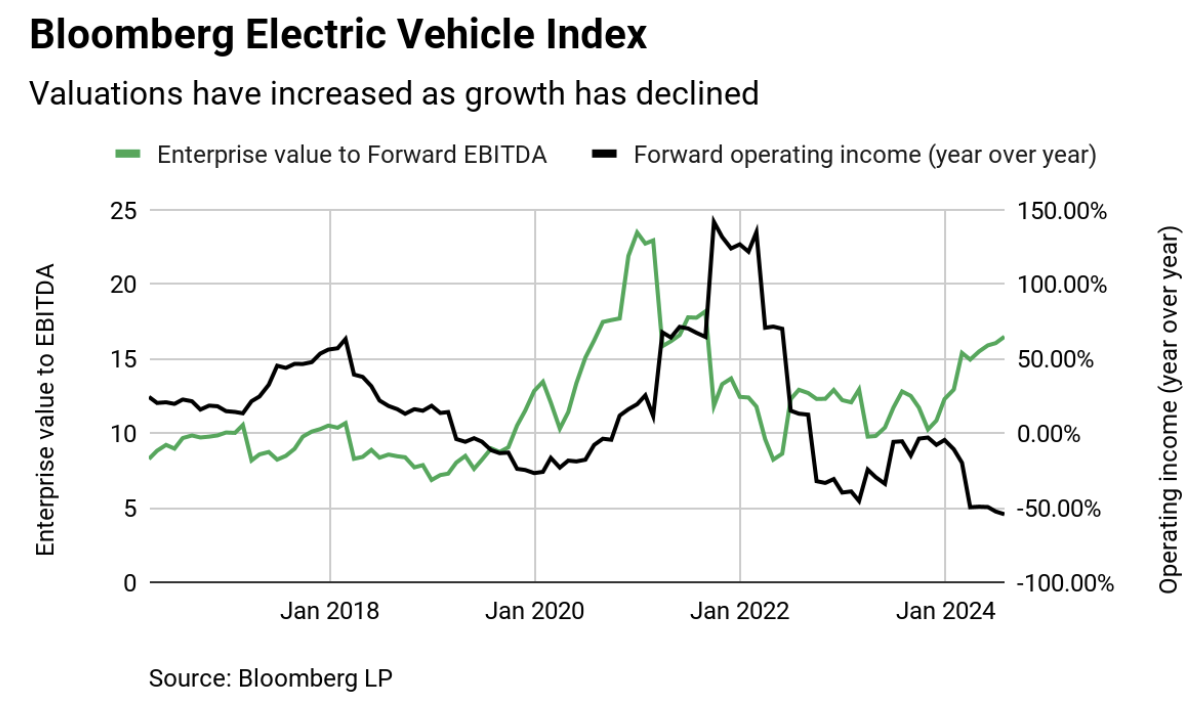

Of course, lower margins can raise questions about valuations. In the chart below, the green line shows the price investors of electric vehicle companies are paying per consensus expected EBITDA (earnings before interest, depreciation, and amortization). Let’s refer to EBITDA as operating income. As you can see, investors have been paying over 15 times operating income, even though the growth in operating income is -50% (black line). The last time growth detracted at this pace, investors paid closer to 12 times operating income. No wonder since its peak in 2021, electric vehicles, as represented by the Bloomberg Electric Vehicles Index, have lost 61.0% of their value (as of 7/29/2024).

While global demand is expected to remain robust, consumer skepticism is presenting new challenges that will likely need to be addressed. So far the industry has responded like many retail companies recently—lowering prices to increase demand. But those companies may still have work to do. My hope is, for our environment longer term, they find a way.