Back towards the 80s? Interest rates could be breaking a three-decade cycle.

Back towards the 80s? Interest rates could be breaking a three-decade cycle.

In the last 12 hours, the universe resurfaced the 1980s for me. Driving on the West Side Highway yesterday, we spotted a 1980 Ghostbusters Chevy. It had police sirens, the little “No Ghost” signs, and a slogan that said “We believe you.” Then, I learned that a Pointer Sisters song from 1982 was recently remixed. The remix came on during my workout early this morning, and with it, a flood of memories related to the song — a scene from my second grade talent show dance popped in my head and Jessie Spano’s breakdown on “Saved by the Bell” (which further cemented my fear of drugs during the “just say no” 1980s).

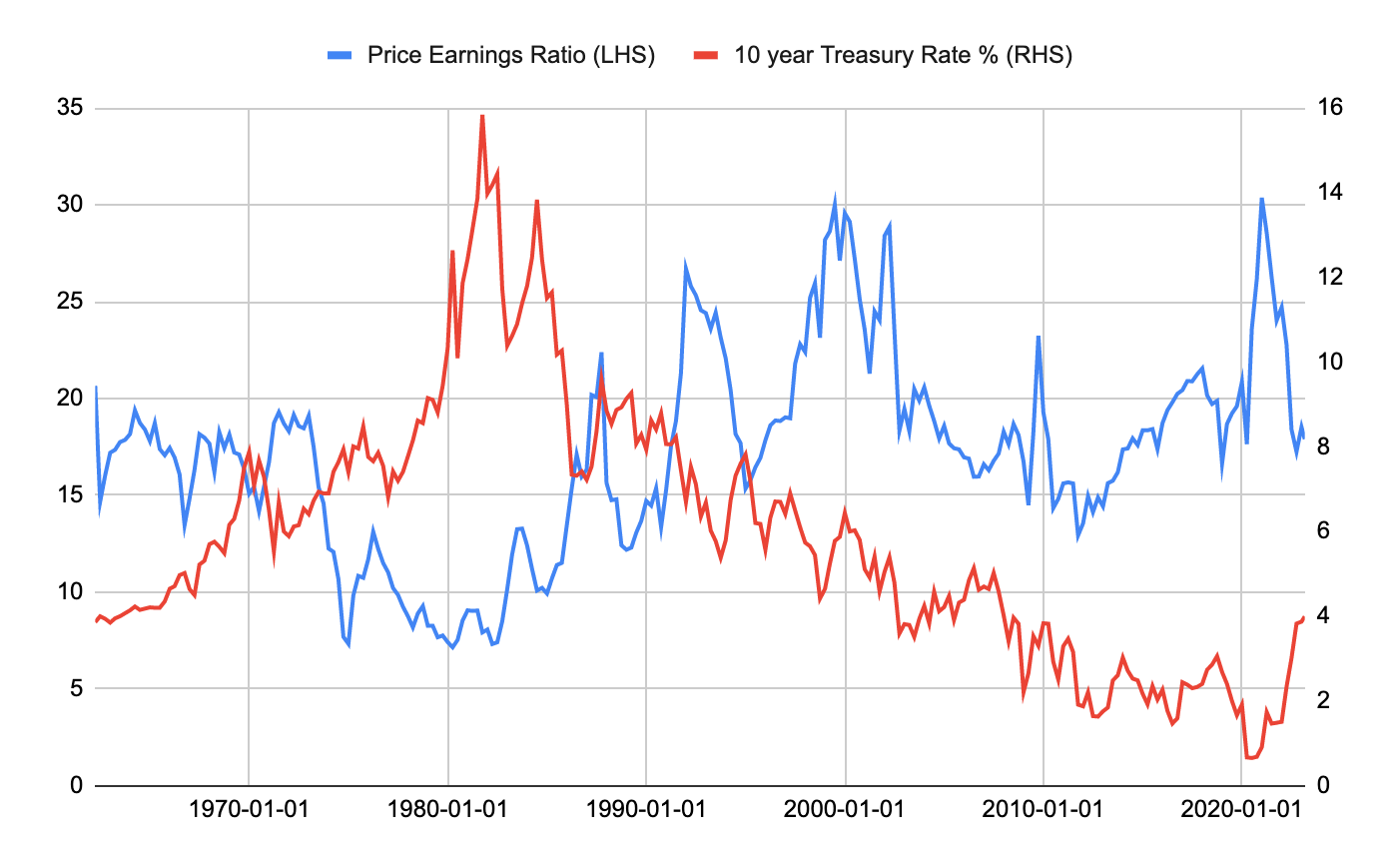

In financial markets, the 1980s were an interesting time. The economy was slowly coming out of a double dip recession and very high inflation. It also turned into somewhat of a hedonistic time in the US — with a focus on wild Wall Street, fast cars, and new technology (like Walkmans) — just watch any 1980s movie. And who could blame them with debt getting cheaper by the decade? Take a look at this chart I have been tracking, which includes the 10-year Treasury yield (in red) and S&P 500 Forward P/E valuations (in blue):

The average 10-year Treasury rate was 10.65% in the 80s. Compare that to: 1990s: 6.1% 2000s: 4.35% 2010s: 2.36%

So far, the 2020s’ 10-year average yield has been 2%... but that’s been grinding higher: now at around 4%. Could it remain sustainably higher in this decade — for the first time since the 1980s? And if so, what’s the implication of that?

Short answers: Yes. Lower valuations and higher hurdles for borrowing.

Longer answers:

1. It’s certainly possible we are in a new regime, where rates are higher on average than the last decade. Drivers of this are both secular (longer term) and tactical.

From a long term perspective, there are three factors to consider: demand, supply, and inflation.

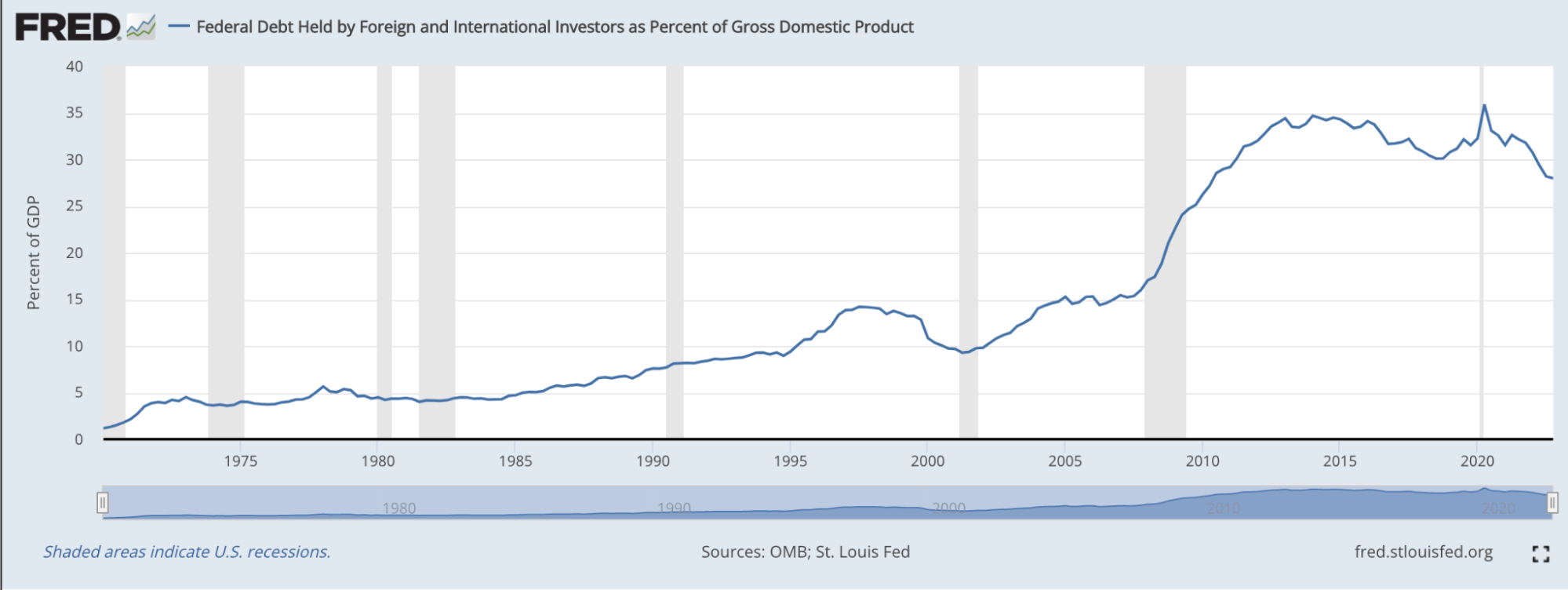

The first is demand for US debt. Non-US investors have been increasing their holdings of US Treasuries for decades, but recently, it looks like that has started to go the other way. With decreasing demand, but the same (or higher) need for the US to borrow, yields could stay elevated. See chart below of US federal debt held by foreign investors as a percentage of GDP.

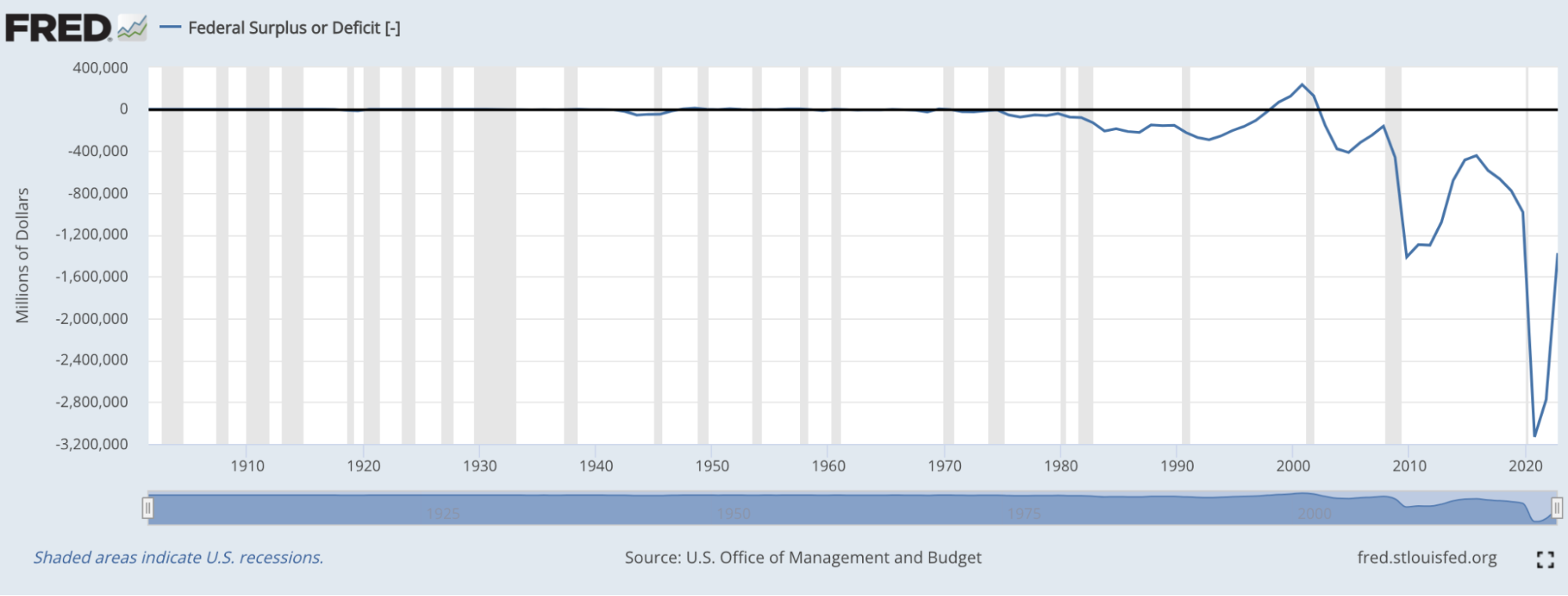

The second, supply — or the need for the US to borrow — doesn’t look like it will change soon. The US has a decent deficit right now. Even though this has recovered some from the lows due to Covid spending, total public debt as a percentage of GDP is over 120% and the Congressional Budget Office expects it to grow by quite a bit. You can see the deficit growth here:

Lastly, a structural shift in the US labor force — due to falling population growth, a rise in the average age, and less immigration — has made an impact on the availability of workers at all levels. Population growth in the 1980s was about 1.25%, while today it’s closer to 0.75%. One real impact from that is on inflation. Lower supply of workers means, all else being equal, that wages must rise, increasing the cost to make and do things.

On the other hand, it’s also possible that rising rates make our debt more attractive, thus increasing demand, and evolving technology reduces the need for labor, offsetting the inflationary effect. Since these are also possible, I wouldn’t say higher interest rates for longer is written in stone, but the probability is relatively decent.

2. So, if rates remain sustainably higher, valuations would likely be impacted further. Harkening back to what I wrote above and at the beginning of the year, the direction and level of interest rates have a direct impact on valuations of most assets. This is because what something is worth is usually considered in light of what it could be worth in the future — and how you bridge that gap is through interest rates. The higher the interest rate, the lower today’s value.

In addition to this general phenomenon, very low rates in the 2010s led to an increase in borrowing — not just by the US federal government but by many entities, corporations, and people. According to the Board of Governors of the Federal Reserve System, non-financial US corporate debt doubled, from just over $6B in 2010 to nearly $13B in 2022. A concern here is when this debt begins to mature, and companies still need to borrow, they’ll have to refinance at much higher rates. That decreases return potential for them, as high borrowing costs reduce profits.

That being said, I also know the markets are built on expectations (not just interest rates). And people can get used to a lot. It’s possible higher rates, that eventually steady, could begin to feel ordinary, leaving the markets to see past them, despite the higher numbers.

Coming back to now, the big near-term macro event arrives this Friday morning, with the February jobs report. Expectations are for an increase of +223K jobs (though some “whispers” expect a bit more). This is a meaningful datapoint on whether the Fed thinks the economy can continue to withstand more interest rate hikes in the face of stubborn inflation.

Longer term, if the Fed (and DJ Powell) manage through the current macro environment even close to right, we should be on a good path to a better economy. I even believe short-term recessionary pain is worth potential falling inflation (and interest rates)... just ask the bond traders from the 1980s.

Sources: Robinhood Financial, Bloomberg, St. Louis Fed