Music sounds better with you: earnings season preview

Music sounds better with you: earnings season preview

Not a flex, but I have decorated my home with quotes from favorite songs. Music has been by my side through tough times and party times. So from The Cure to Biggie to Cardi B, I feel it’s only right to honor it, and let the poetry of the words remind me that I’ve not only gotten through 100% of my days, but even danced during some of them.

We are almost through the tougher market quiet period typical of this part of the year, so it’s time to get ready to dance with Q1 earnings season kicking off on Friday morning with the banks (plus some inflation data this week with CPI today and PPI tomorrow).

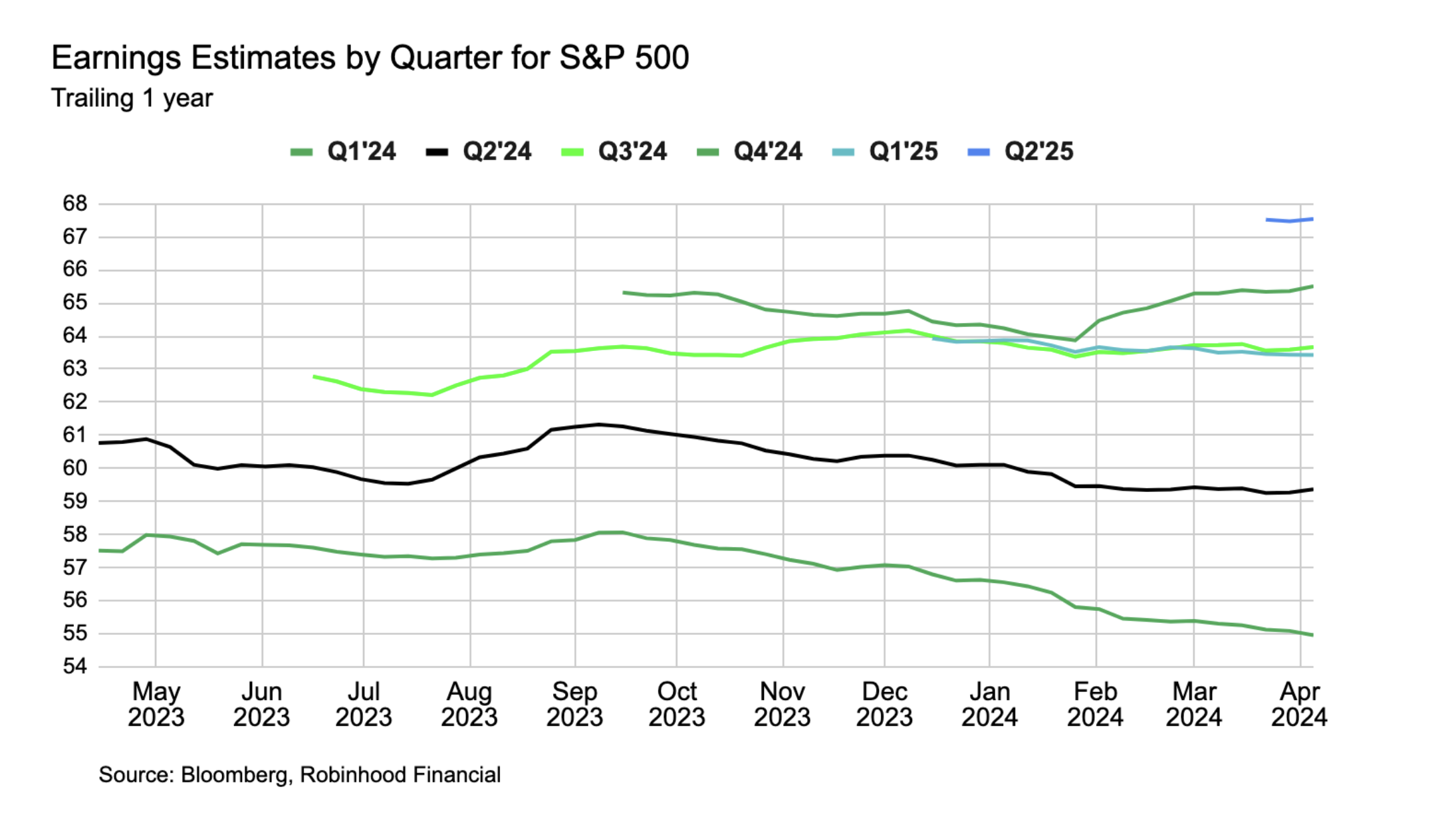

Right now expectations are for S&P 500 earnings to increase 3.2% y/y in Q1, which fell by 2.5% over the last three months (see chart below). A drop in expected earnings growth is common heading into the start of earnings season, though this time it's by about 1% less than the average drop over the last 5 and 10 years (according to Factset Earning Insights). Full year 2024 earnings growth is expected to be about $244 per share, which is about 11% higher from 2023 earnings.

Remember, earnings growth is correlated to stock prices over time. And in the short term, there is often a correlation between stock prices and the difference between expected earnings and actual earnings.

What will I be watching for during this earnings season? For the whole season, it depends on the sector, but here are a couple things to start:

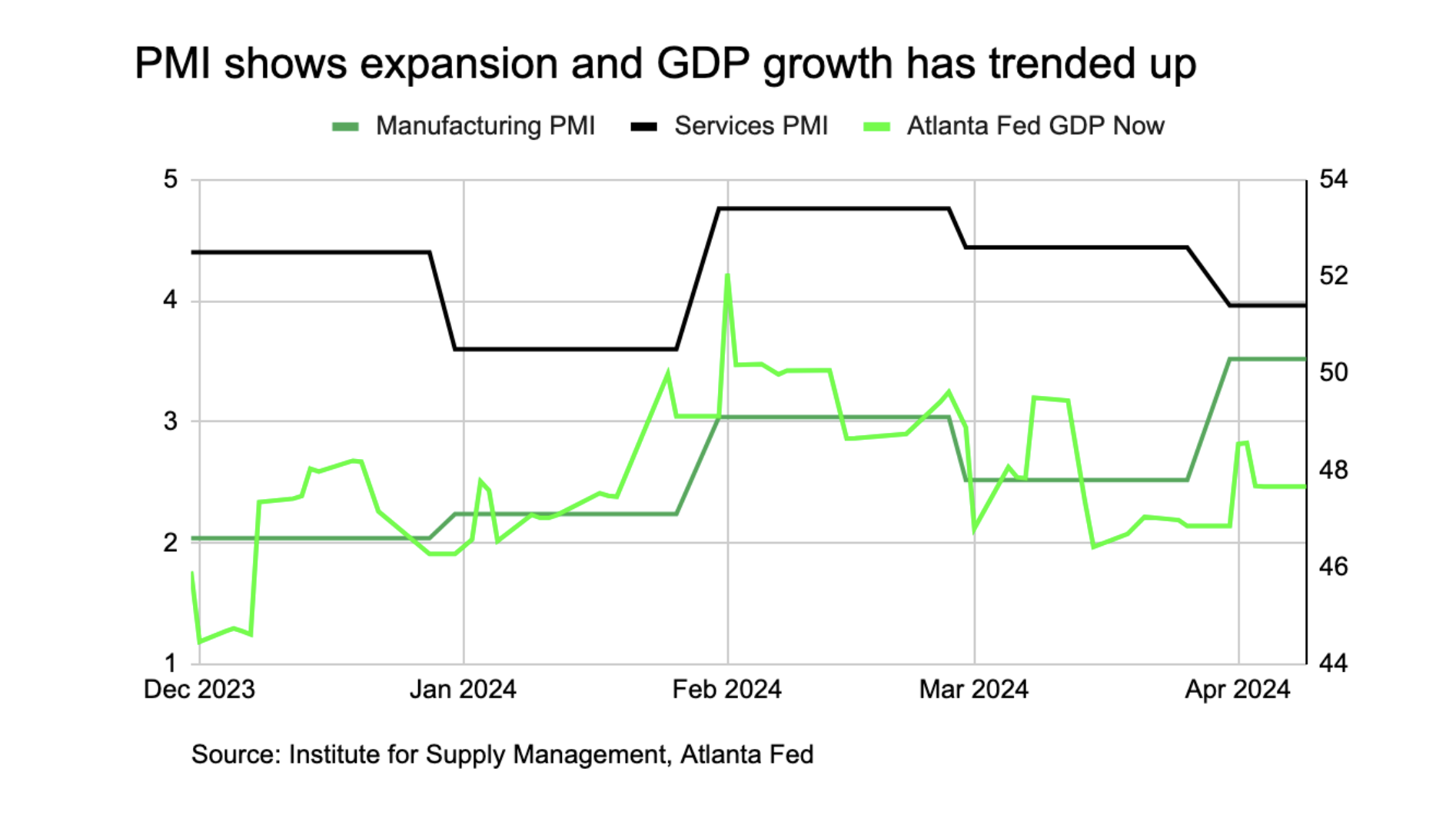

Expectations relative to what is stated: Q4 earnings seasons showed a decent trend of companies providing Q1 and 2024 guidance below what was expected (aka “negative guidance”). For example, according to Factset, of the 112 firms that provided guidance for Q1, 71% issued negative guidance. When this happens, even if earnings reported were strong, the stock price typically falls. So I will be very focused on what the Street thinks guidance should be and what it ends up being. I do think we could see better guidance this quarter than last, which should bode well for the markets. Certain indicators, such as those in the chart below, have improved over the last 3 months—like ISM Manufacturing PMI improving from 51 to 53, Services PMI increasing from 50 to 51, and GDP expectations increasing from 2% to 2.5% over the quarter.

Banks are kicking off the season on Friday (e.g., JPMorgan, Citi, State Street and Wells Fargo are the big banks reporting): According to FactSet, banking earnings are expected to show a decline of -18% y/y in Q1 vs. a 3.2% increase for the S&P 500, with regional banks expected to look worse than the big banks. Commercial real estate loans they hold will continue to be a hotspot, but more interesting to me, given the poor earnings and guidance from retail companies, is their take on the consumer. Other things to look out for are net interest income given the competition for deposit savings and any color on the impact it’ll have on their businesses if the Fed doesn't lower rates very much this year.

What song will earnings season sing—dance or the blues?