The effects of past choices: risk vs. reward in a world of higher interest rates

The effects of past choices: risk vs. reward in a world of higher interest rates

We make choices everyday. We choose our clothes, the food we eat, and people we stay connected to. Choices that you know may not be good for you, like eating a donut or wearing high heels, are made because the downside (sugar, calories, bunions) is worth it.

Equally, investing and running a business involve many choices. When investing, there are choices about which assets – stocks, bonds, options, commodities, etc. – to invest in. And then, there are even decisions about the way investment decisions will be made. Will you use technical analysis, where charts are analyzed to make decisions, or will you focus on fundamentals, like earnings forecasts and valuation ratios, to decipher what is attractive? Or both? Or just your gut?

Some of it depends on the time horizon, where technical analysis can be effective in the near time while fundamentals tend to be effective in the very long term. But, what I do know is that over time, cash flow (earnings or otherwise), growth, and interest rates drive the direction of prices of almost any asset.

When interest rates are very low like they were in 2020 and 2021, whether an asset, such as a stock, provides actual earnings and cash flow can matter less to investors as long as there is expected growth. That’s because in low interest rate environments, the cost to borrow to invest is very low, while the opportunity cost to not invest can be high (meaning, you don’t get much out of cash sitting in a savings account). Another way to think about it is when interest rates are near 0%, cash earns little value — so the potential return for anything else doesn’t have to be as high. As we’ve seen in many previous periods, including last year, this can lead to risk being underestimated. In short, easy money can make risk feel, well, less risky.

Inevitably though, the tide rolls out and you get to see who took on too much. Today, with interest rates higher, money (like a lot of things) costs more now. Any company that may have overextended themselves will likely start to come under pressure or break. And scrutiny from investors will likely be greater. What’s happened with FTX is the most recent example of what appears to be risks created without transparency, coupled with the cost to borrow being very low (maybe for too long). In the past, there have been others: the dot com bubble in the late 90s, the mortgage crisis in 2008, Enron, AIG, to name a few.

It’s why our team has been so focused on earnings and quality. With interest rates now much higher than they were, and our view that they will remain elevated, even if inflation comes down more than the bit it has, earnings (positive profits) and expected growth rates have become that much more important. For a while, we felt the market had maintained elevated expectations of earnings (and thus growth) well beyond what made sense, despite a very different environment than last year.

Let me show you what I mean:

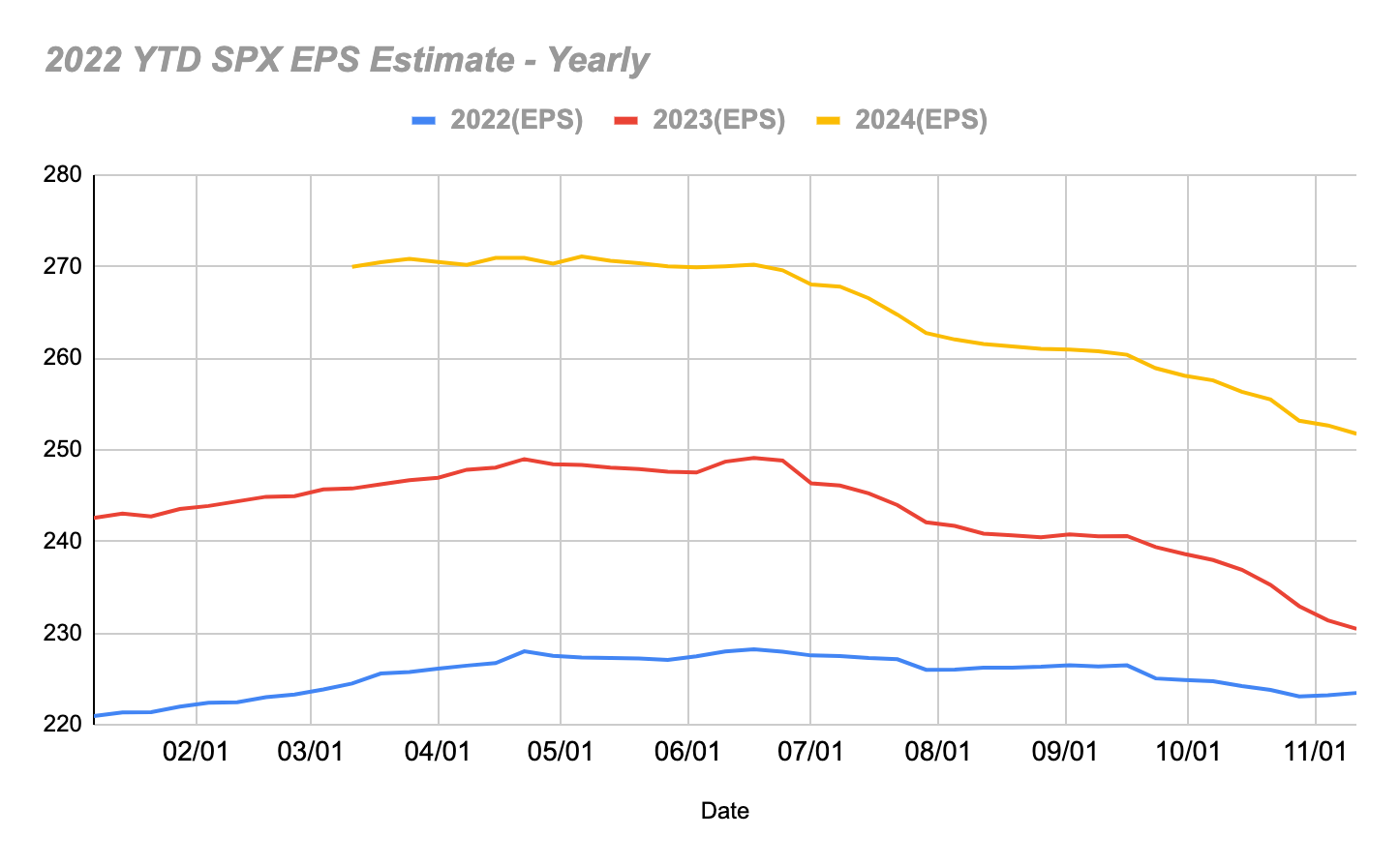

Source: Bloomberg

Because the markets always tend to look ahead to next year, let’s focus on the red line, which represents 2023 earnings. You can see above that expected earnings for 2023 for the S&P 500 Index, were expected to be around $250 per share between May and July. Those estimates would have meant, based on 2022 expectations, that earnings would be growing 9% each year, for this year and next year — despite all the stuff that has happened: high inflation, rising interest rates, war, and Covid still prevalent. Keep in mind, the average annual earnings growth rate since 1947 is 7.5%. All this is to say that we expected earnings estimates to fall, and they have. Today, they’ve dropped by $20 per share to $230 per share — and they just so happened to do that during each of the earnings reporting seasons (July and October). While it’s much closer to our own estimates of $220 to $230, it’s still a bit elevated.

In fact, valuations — when you take the current level of the S&P and divide earnings expectations for next year (aka the 1-year forward price/earnings ratio) — still look expensive. The S&P, which is at around 4,000 now, divided by $230, gets a 17.4x multiple. That is much higher than the long term average of 16x (especially when rates are higher).

But if there is one thing I have learned in my career, whether valuations are fair or not can take awhile to matter.

So, the market has a pep in its step right now. The macro overhangs (that we know of!) have started to look better, inflation is a little cooler, China is easing their Covid restrictions, Ukraine took back their city of Kherson, and the Fed looks closer to pausing interest rate hikes than they have all year.

But, back to choices: I believe the risk that remains is in the investment and corporate sector. That’s where the bulk of the recession, which we believe has already started, will be felt, IMO. The free money period created excesses — an excess of net profits not mattering — and some still need to be fully corrected. That means many companies will likely continue to make tough choices themselves — with layoffs and/or cost cutting. Thus, earnings in areas that may have been overleveraged, may still need to fall before they are in the clear.

In the short term, perception can matter more than valuations, which is why the market risks should stay skewed to the upside for now. I think valuations and earnings growth will start to matter again during the next earnings season in January.

Until then, enjoy the holiday season. New Year’s resolutions about better decisions will be here before you know it.