Pictures can say a lot (about the markets)

Pictures can say a lot (about the markets)

Sometimes you get a question from a friend, partner, or colleague that is so loaded for you, you just can’t get an answer out. As if the prospect of clearly explaining your thoughts is so exhausting, that you opt to say it’s too much to get into, or distract the inquirer from the question with a question to them.

That’s how I feel about the markets, and the economy, right now. A swirl of thoughts and connections hit such that I can’t find my way out of it. BUT, data, charts and pictures can be the thing that provides clarity when you can’t find the words—the thing that allows you to simply say, “see?”.

So I give you the current market sitch in four charts (with light explanation):

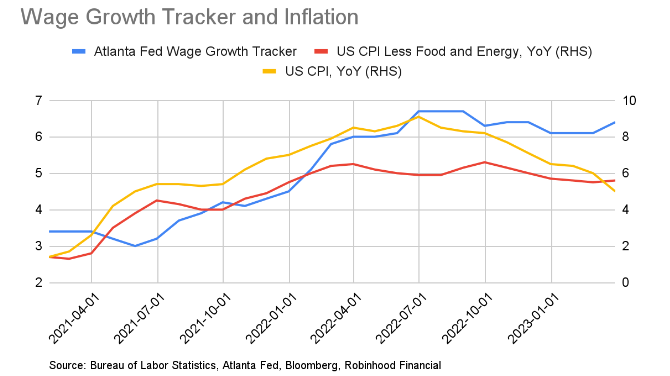

1. Inflation is still the Fed’s boss and the Fed is still our boss. Inflation has come down in many places (in “goods”), but not everywhere (like “services”). One key area of concern for the Fed is wage inflation. The longer this stays high, the more likely inflation will stay elevated, because demand will not fall enough for prices to fall in the most stubborn places. Thus, the Fed will see a need to keep interest rates higher to slow down the economy, risking a recession. Below is a chart of wages, in blue, and inflation, both headline and core, in yellow and red, respectively.

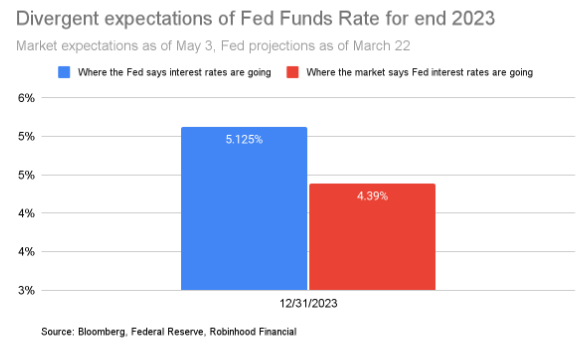

2. The market thinks the Fed will drop interest rates in the next few months but the Fed doesn’t yet agree. Given the above, it’s not a foregone conclusion that they will lower rates. And, at their last Fed meeting, they stated they expected their own rates to stay around current levels until at least next year. With the Fed’s next statement and conference call starting at 2 PM ET, where they are expected to raise rates by 0.25% to ~5.125%, it will be a highly watched event, for what they will say about the future, given this discrepancy.

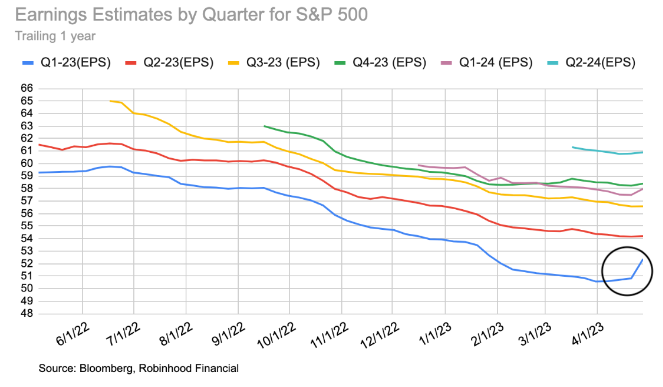

3. Earnings have been stronger than expected on the whole. Now that we are more than halfway through the earnings season for Q1 '23, it's clear that expectations fell too far heading into it. Companies have been able to beat earnings estimates on the whole and, as a result, they have increased for the remaining companies still to report. However, keep in mind, earnings are still contracting—around -6% YoY—but they hurdled over the low expectations. This is in contrast to weakening economic conditions.

And it’s not often you see earnings doing better than expectations, while economic data is also softening. However, I did recently see margin sentiment data—meaning an analysis of company management team views on their profitability—has fallen, reflecting how the slowing economic growth could pressure future corporate margins.

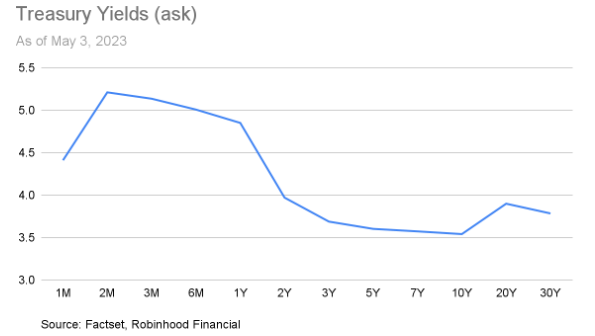

4. The debt ceiling is coming. We are very close to not being able to fund the government after reaching the current debt ceiling of $31.4 trillion earlier this year (I wrote about this last week as well). On Monday evening (May 1) we got an updated estimate on how much time—or money—is left before the US government is no longer fully funded. The date was estimated to be on or around June 1. This is on the earlier side of expectations and now forces real discussions between Congress and the President to come up with a solution (we believe it’s likely a temporary one at first in the form of a suspension). In line with our own expectations, the markets did not like the shortened timeline and t-bills (short term treasury bonds) that mature around this date have much higher yields than treasury bonds maturing in two years or longer, reflecting the risk right now.

I guess I did end up writing my thoughts down here… but the pictures helped me get there. And despite the clear pictures, the Fed and the market are still very data dependent, with clarity on the low end of the historical range. But so far, US companies have navigated the uncertainty well—though they are also becoming less certain of their future.