Noise vs. news

Noise vs. news

The volume has to be turned way up in the morning. Watching TV Monday evening had me at soft volumes—as low as 11 on my Sony. But turn it on the next day, and I can barely hear it. I’m sure a scientist can confirm this, but your brain must be more sensitive to sound on Monday nights vs Tuesday mornings.

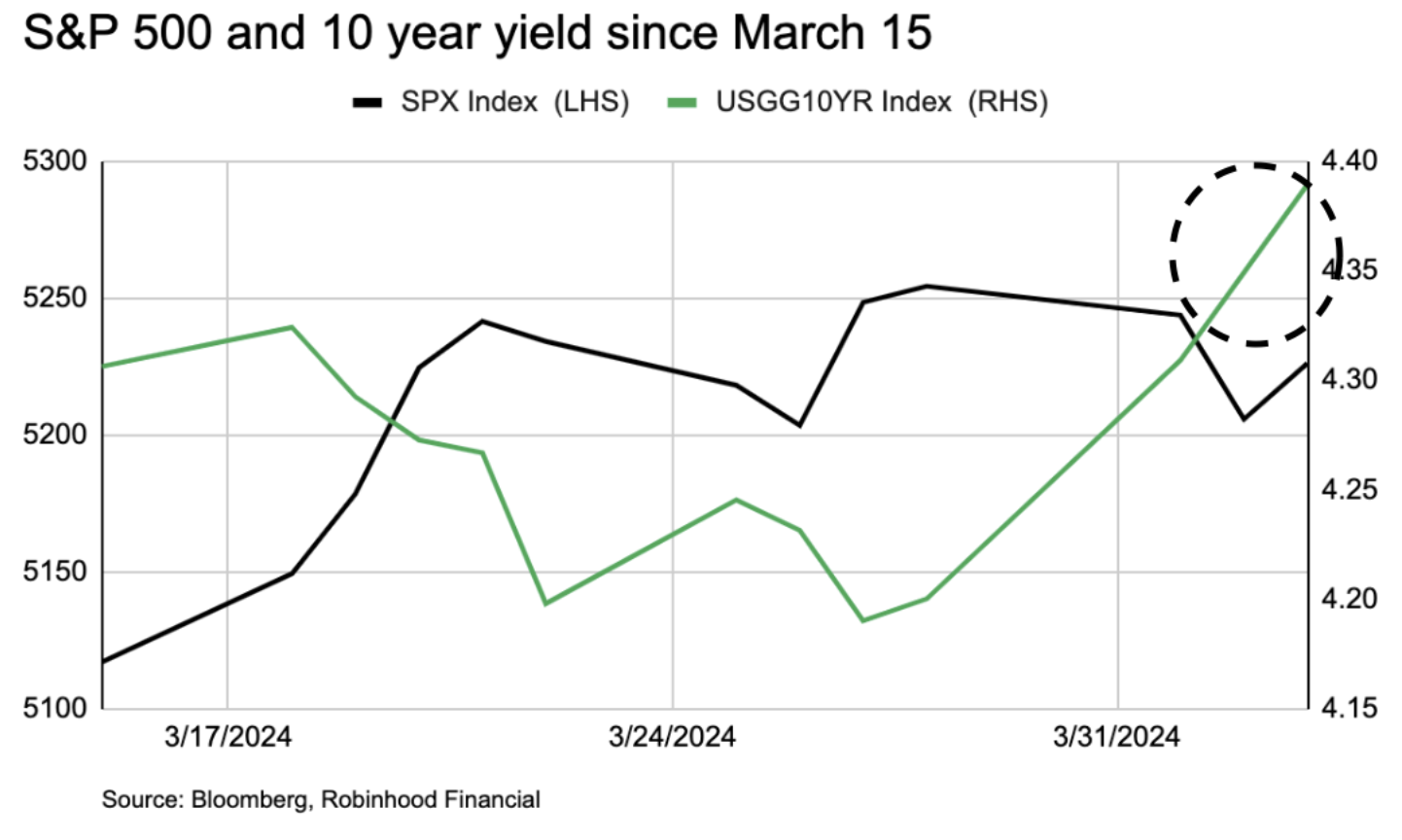

It’s like this week in the markets. It’s a little more sensitive to what’s usually a little bit of noise. Monday’s ISM Manufacturing came in higher than expected—which shows better growth and higher prices. But the market didn’t like that. Stocks ended lower that day, particularly in the interest rate-sensitive sectors like financials, and the 10-year treasury rate increased (which the market also didn’t like). See chart below for that move.

This is because it doesn't want higher growth or higher prices. It wants lower growth, lower inflation and, thus, lower interest rates from the Fed. You can’t blame it — we all want lower inflation and interest rates. But the desire for lower growth is atypical. And usually ISM Manufacturing data, in general, gets a quick glance, not a major reaction.

The thing that does matter, which we’ll get an update on this week, is the labor market. As I’ve shared before, I think jobs data is key to whether we get a soft landing in our economy—or a not-so-soft landing.

Tuesday brought the “Job Openings and Labor Turnover Survey” (JOLTS) data. This showed 8.756mm job openings, which is only slightly lower than expected and close to the same as last month.

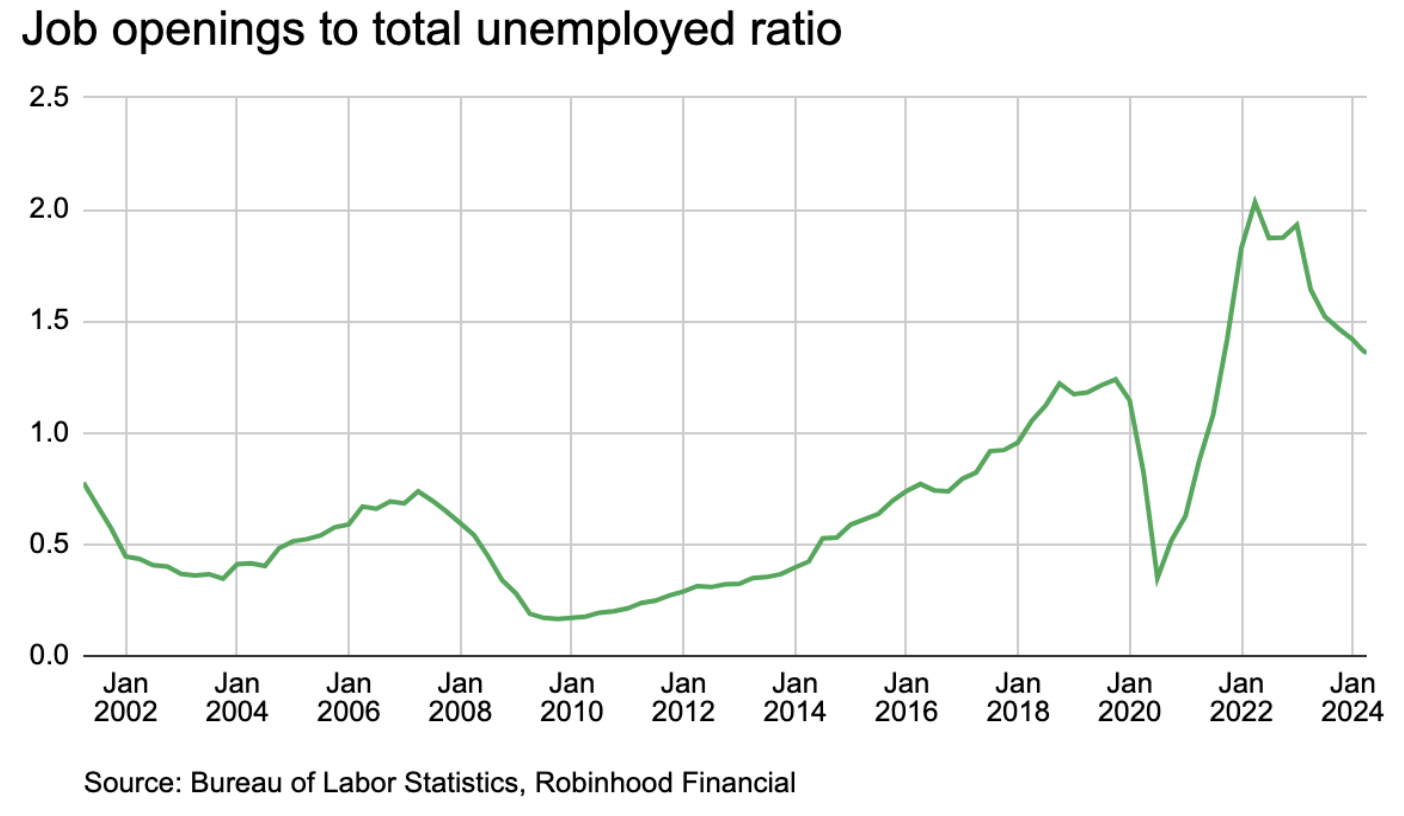

An interesting measure using this data is the total openings to unemployed ratio. It’s essentially a gauge of labor market tightness—meaning how hard it is for companies to find workers, or not. The higher the number, the more openings there are vs. people looking for work. It’s currently at 1.36, down from a peak of 2.0 in March 2022, and much higher than the median of 0.59 going back to 2001. So relative to history, it’s still tougher for companies to find workers than the last two decades.

On Friday, we’ll get the other employment data for March: non-farm payrolls, unemployment rate and hourly earnings growth. Consensus expects the report to say 205,000 jobs were added, the unemployment rate is 3.8%, and annualized wages grew by 4.1%. Anything stronger than these numbers will likely be unwelcome–similar to the thinking that strong growth will mean higher interest rates.

Though, I am focused on two data points when it comes to Friday's report:

The household survey that comes out, which tracks the number of people employed vs the number of jobs added and

Whether or not the unemployment rate gets into the 4’s (it was 3.9% last month).

I think both are a good tell of the growth of the economy and progress towards a soft or not-so-soft landing. If people stay employed, a strong economy, and some of the things that come with it, shouldn’t feel too bad.

The rest of the data is closer to noise.