What is Simple Interest?

Simple interest is a basic way of calculating interest that doesn't account for compounding that is, interest that accrues on interest that was charged.

🤔 Understanding simple interest

When you deposit your money in a bank or credit union savings account, they will pay interest on that amount. Typically, the interest that is paid is calculated using sophisticated methods that include compounding of interest. Simple interest is a straightforward calculation that gives you a quick estimate of the amount that you'll owe (or that you’ll receive), without using complicated formulas. All you need to know is the principal amount, the interest rate, and the length of time between each payment. You can also use simple interest to calculate how much interest you'll earn from a savings account.

Let’s say you want to open a savings account and have to decide between 3 different choices:

- 0.5% interest, no monthly fee

- 1% interest, $2 monthly fee

- 2% interest, $5 monthly fee

You can use the simple interest formula to figure out roughly how much you'll earn each year and whether it makes sense to pay a monthly fee. If you're depositing $5,000, the accounts will pay roughly:

- $25 each year

- $50 each year

- $100 each year

In reality, you'll earn slightly more due to compounding, but simple interest is enough to get a basic idea of your options.

After subtracting out the monthly fees, you can see that you'll earn a net of:

- $25 each year

- $26 each year

- $40 each year

This means that choosing the third account will let you earn the most interest. If you had less than $5,000 to deposit, you could use the same calculation to figure out if a different account would be a better choice.

Takeaway

Using simple interest is like getting an estimate for a home improvement project…

You ask a contractor to give you an estimate of how much it will cost to remodel your kitchen. The contractor uses some quick and easy math based on labor rates and the cost of raw materials to give you a number. You know that the number isn't exactly what you'll owe, but it's close enough to reality that it's useful for making decisions. In the same way, using simple interest won't give you the amount of interest you'll earn down to the penny, but it's close enough to be a useful measure and is easier to calculate.

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock. Securities trading is offered through Robinhood Financial LLC.

What is simple interest?

Simple interest is interest that is based purely on the balance of an account. Interest isn't assessed based on the interest that has already accrued in the account. This differs from compound interest, where you would pay or earn interest on the interest that accrues each month on top of the original balance of the account.

Calculating simple interest is much easier than compound interest, which makes it useful for approximating the interest that you'll earn or owe when you're looking at different financial accounts. In reality, the majority of deposit accounts use compound interest. The usefulness of simple interest also tends to break down over time. For example, ignoring compounding when calculating the ending value of a savings account in 10 years would ignore a significant benefit.

What is compound interest?

When a deposit account uses compounding interest, interest accrues based on both the balance and the interest that has already accrued. If you deposit money to an account that pays interest, you want the interest to compound. Compounding interest means that you'll earn based on your initial deposit and on the interest that you've received, speeding the account's growth.

If you're borrowing money, compounding interest means that you'll pay more for the loan. If you lend money, you'll earn more interest with compounding interest.

When calculating compound interest, you need to keep the compounding period in mind. The compounding period is the frequency with which interest compounds. More frequent compounding means interest accrues more quickly.

For example, if interest compounds monthly, interest will be added to the balance of the loan at the end of each month, and interest will begin accruing on the original balance plus the accrued interest.

Typical compounding periods are daily, monthly, quarterly, and annually.

Often, companies will quote their interest rates in annual rates but will compound more frequently than that, leading to a higher effective interest rate. For example, credit cards often list their rates as annual percentage rates but compound their interest daily.

How is simple interest different from compound interest?

Simple interest accrues only based on the principal of a loan. Compound interest accrues based on both a loan's principal and any interest that has already built up. This means that you pay interest on interest when using compound interest and do not pay interest on interest when using simple interest.

Consider this example:

You borrow $100,000 from a bank at an interest rate of 5% per year. You don't have to make any monthly payments but must pay the loan in full at the end of three years.

If the loan used simple interest, you would pay $15,000 in interest — 5% of $100,000 is $5,000, and $5,000 each year for three years totals $15,000.

If the loan uses annually compounding interest, the balance of the loan after year one will rise to $105,000. In the second year, you would pay $5,000 on the original $100,000 balance, plus $250 in interest on the $5,000 that accrued, making your balance $110,250. After the third year, your balance would rise by another $5,000, plus 5% of the $10,250 accrued interest, resulting in an ending balance of $115,762.50.

Compounding interest makes total interest payments grow more quickly. Similarly, compounding interest makes account balances grow more quickly if you deposit money to a bank account that pays interest, such as a savings account. In short, if given a choice, you want to pay simple interest when borrowing money and compounding interest when lending money.

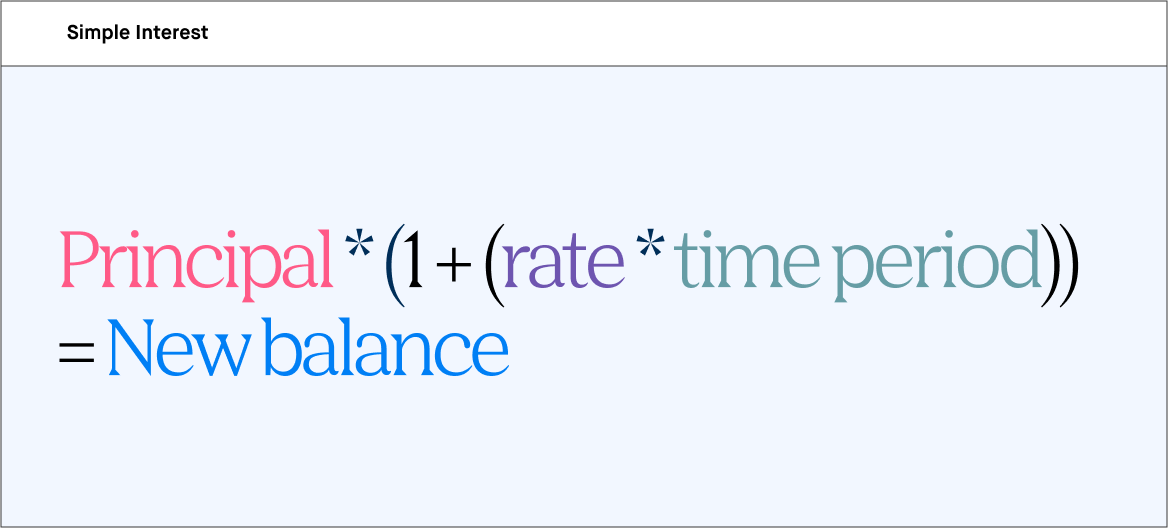

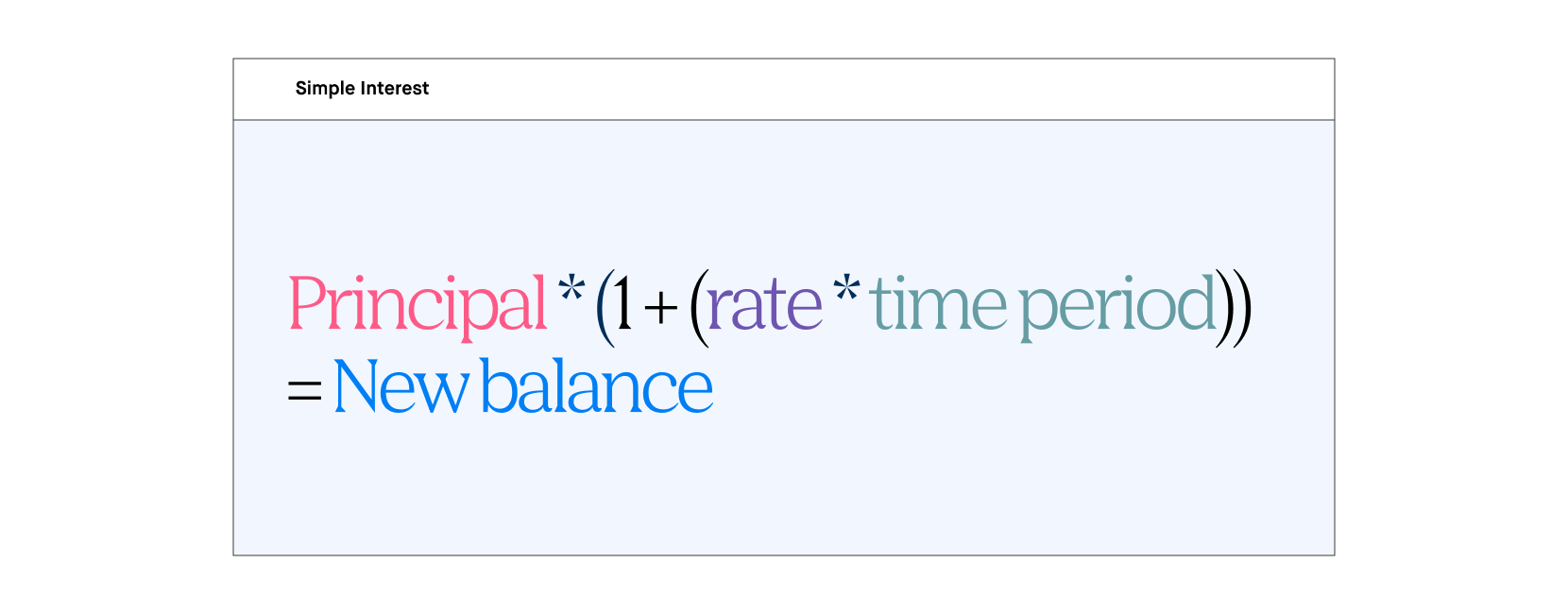

How do you calculate and interpret simple interest?

The formula for simple interest is:

For example, if you deposited $10,000 to a bank account that pays 2% simple interest each year, at the end of the first year, you’d have:

At the end of two years, you would have

Because the interest doesn't compound, you earn the same amount of interest each year.

In reality, the majority of bank accounts and loans don't use simple interest. But, you can still use the simple interest formula to estimate the interest that will accrue — Just remember that the actual amount should be slightly higher.

How do I calculate compound interest?

Compared to calculating simple interest, calculating compound interest is more complicated. That's why people often use simple interest to estimate the amount of interest that will accrue.

The formula for calculating compounding interest is:

So, if you deposited $10,000 to a bank account that pays 2% interest per year, compounded daily, you’d have

After two years, you’d have

If interest compounded monthly instead, after two years, you’d have:

Typical compounding periods are daily, monthly, quarterly, and annually.

Is simple interest good or bad?

Simple interest isn't inherently good or bad. It's just another way of calculating interest. However, whether it benefits you is dependent on whether you're borrowing or lending money. Typically, simple interest benefits borrowers. By only charging interest on the principal amount, simple interest charges less interest overall than a loan that uses compounding interest. That means that borrowing money is cheaper. If you're getting a loan, getting a loan with simple interest may help you save money.

If you're lending money — including by depositing it to your savings account or by buying a bond — you'll earn more interest with compounding interest. The more frequently the interest compounds, the more interest will accrue on the loan or in your bank account.

In general, simple interest is good for borrowers, while compounding interest is good for lenders.

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock. Securities trading is offered through Robinhood Financial LLC.