What is a Credit Score?

A credit score is a number assigned to an individual by businesses called credit bureaus, that lenders use to gauge the likelihood that an individual will default on a loan.

🤔 Understanding credit scores

A credit score is a numerical score that lenders use to get a basic idea of how likely a borrower is to repay a loan. Credit bureaus, companies that track consumers and their interactions with credit, assign credit scores to individuals. When lenders lend money to consumers, they’re doing so with the expectation that they will be paid back and earn a profit by charging interest. If a borrower doesn’t pay the loan back, the lender loses money. This means lenders generally prefer to give loans only to people who are likely to make their required payments. Credit scores range from 300 to 850, with a higher score meaning a borrower is considered more likely to repay his or her debts.

When you apply for a loan — say, to purchase a car — the lender will most likely check your credit before making a lending decision. To do this, the lender will ask a credit bureau for a copy of your credit report. The report includes information about all of your loans and credit cards and the payments you’ve made on them. Your credit report also includes a number, your credit score, derived from the information on your report. Based on your score, the lender can categorize you as having poor, fair, good, or great credit, and use that information as part of the basis of its lending decision. In the example where you’re applying for a car loan, you may be offered better or worse lending terms depending on whether your credit is considered good. If your score is, say, 800 (on the high end), you may be offered a lower interest rate and overall better lending terms.

Takeaway

A good credit score is like having a character reference…

When you’re meeting a new group of people, it can be helpful to have someone who knows you and the group that you’re about to meet. Your acquaintance can introduce you and tell the group a bit about you. Because the group trusts your acquaintance, they’re more likely to trust you. Similarly, credit bureaus serve as a character reference when you apply for loans – Giving lenders your credit score helps them know whether you’re trustworthy as a borrower.

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock. Securities trading is offered through Robinhood Financial LLC.

What is a credit score?

A credit score is a numerical score, ranging from 300 to 850, that lenders use to gauge whether they should offer loans to consumers. Credit bureaus collect and track consumers’ credit information, including the number and type of loans, their balances, and their payment history. Using this information, credit bureaus produce credit reports and calculate credit scores for consumers.

By far the most commonly used type of credit score is called a FICO score — It gets its name from the company that developed it, the Fair Isaac Corporation. (There are other credit scoring systems, but your FICO score is more or less synonymous with your credit score.)

You can think of a credit score or FICO score like a weighted GPA from the grades on someone’s report card. Add up the values of the person’s grade in every subject and factor in how difficult or important those classes are. An advanced level course might be worth more than an intro-level course. Similarly, credit bureaus weight different aspects of your credit report and use those weights to calculate your credit score.

When you apply for a loan, most lenders ask one or more credit bureaus for a copy of your credit report and credit score. They typically look at the details of your report but use your credit score as a quick and easy way to gauge your creditworthiness. High credit scores indicate borrowers that are more likely to repay their loans, while low scores indicate higher-risk borrowers.

Why is a credit score important?

Credit scores are important because they impact many aspects of consumers’ lives, including their ability to qualify for loans and how much they pay for those loans. When lenders offer loans, they usually want to be sure that they’ll get their money back, plus any interest they charge. Ultimately, lenders want to make money by lending money, so offering loans to people who won’t pay them back is a bad idea.

Having a good credit score means that lenders will tend to be more willing to offer you a loan. There are many factors at play in lending decisions, but your credit score is one of the most important ones. If you have bad credit, few lenders will be willing to offer you a loan.

Once you qualify for a loan, your credit score also impacts the amount that you’ll pay for the loan. People with higher credit scores tend to have lower interest rates on their loans than people with lower credit scores. Lenders compensate for the increased risk of lending to people with low credit scores by charging them more in interest.

For long-term loans like mortgages, the effect of a good credit score, and the resulting lower interest rate, can be huge.

A $100,000, 30-year mortgage at 4% interest will cost a total of $171,870. If someone with a lower credit score applies, they may only be able to borrow money at a rate of 4.5%. They’ll pay a total of $182,407. In this example, better credit can save someone nearly $11,000 on a $100,000 loan.

Depending on local laws, credit score also impacts consumers’ ability to rent an apartment or open a new account for utilities, cable, internet, or cellular service.

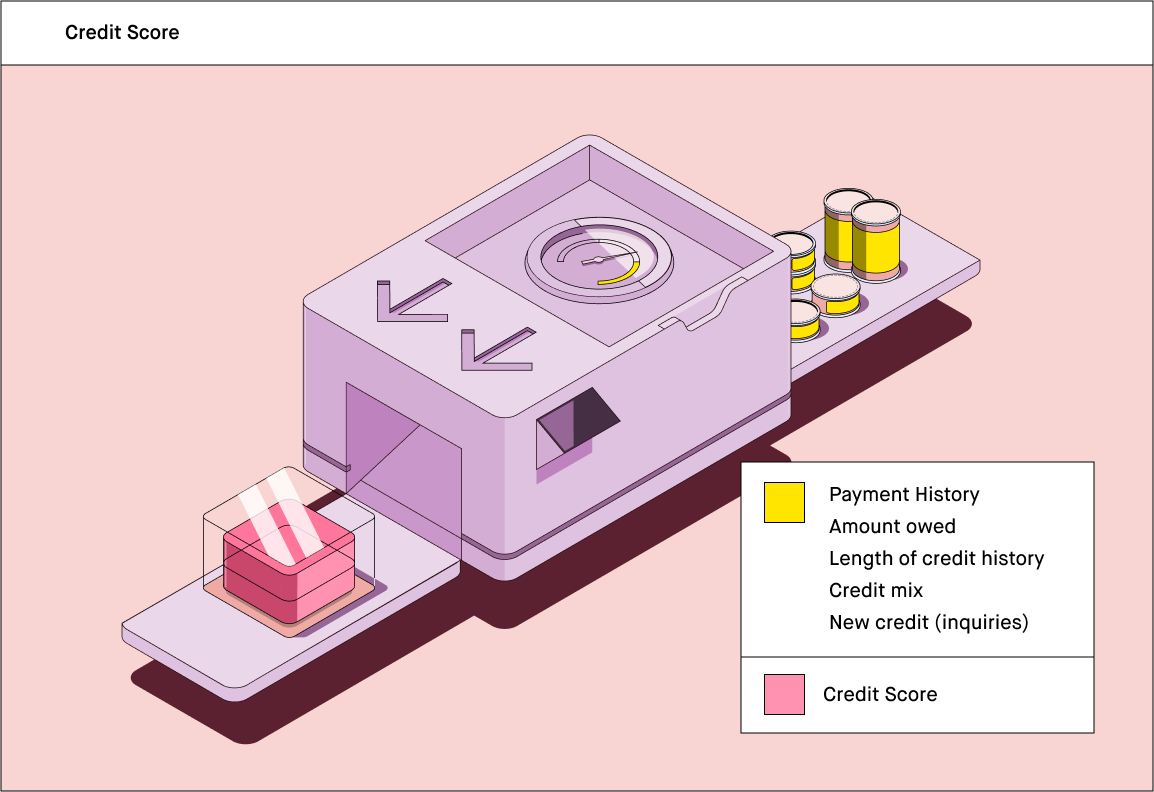

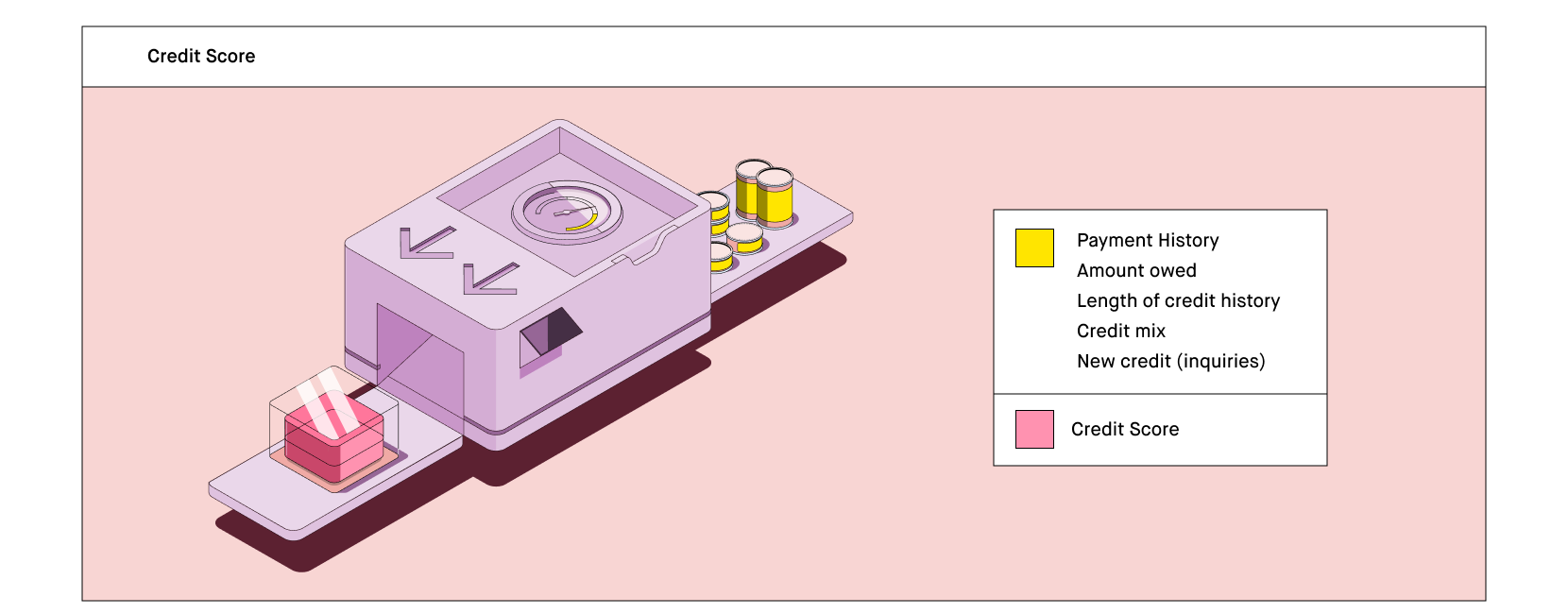

What factors affect credit score?

Five factors make up your credit score:

- Payment history

- Amount owed

- Credit mix

- New credit

- Length of credit history

Payment history

Payment history is the most important part of your credit score. This is your history of making required payments. Every on-time payment helps your score, while every late or missed payment hurts your score.

Missed payments tend to have a more substantial effect than on-time payments. It can take months or years to restore your credit score to its previous level after a missed payment, even if you make every payment going forward.

Amount owed

This factor includes both the simple amount that you owe as well as your credit utilization. Generally, the more you owe, the lower your score will be.

Your credit utilization is the ratio of your total revolving debt to the total credit limits of all of your credit cards and lines of credit. Typically, people who rely heavily on rotating credit and who carry a balance on their cards or lines of credit are riskier lending prospects than people with low utilization. This means that a high credit utilization ratio typically leads to lower credit scores.

Credit mix

Experience with debt doesn’t just mean having dealt with it for a long time. It includes handling different types of debt, including student loans, credit cards, mortgages, or auto loans.

Usually, having multiple types of loans appear on your report leads to a higher credit score than if you just had one kind of loan.

New credit

When you apply for a loan, lenders usually ask a credit bureau for a copy of your credit report. When credit bureaus receive this request, they make a note of it, adding that note to your report. This is called a hard inquiry.

Every hard inquiry drops your credit score by a few points. Lenders tend to see frequent applications for credit as a sign that you need to borrow money and might have financial problems, putting you at a higher risk of default.

Length of credit history

Typically, the more experience that a person has with credit, the better they are at handling credit and debt. The longer you’ve had access to credit, the higher your score tends to be.

This factor also includes the average age of your credit. Lenders usually like to see borrowers that build long-term relationships with their lenders. The older your average line of credit is, the better it will be for your score. This makes it important to keep old credit lines open, even if you don’t use them.

How is my credit score calculated?

The formula for calculating a credit score isn’t public information. Credit bureaus use complicated formulas to calculate your credit score based on your credit report.

Your score can be roughly broken down as:

- Payment history - 35%

- Credit utilization - 30%

- Length of credit history - 15%

- Credit mix - 10%

- New accounts - 10%

What is a good credit score?

While every lender is looking for a different type of borrower and makes its own lending decisions based on your credit report and credit score, credit bureaus provide rough credit score ranges. You can use these ranges to get an idea of how good your credit is.

For example, Experian, one of the major credit bureaus, offers these ranges:

- Very poor: 350 - 579

- Fair: 580 - 669

- Good: 670 - 739

- Very good: 740 - 800

- Excellent: 800 - 850

What is a good credit score for my age?

Because the length of your credit history and the number of on-time payments that you’ve made is a significant component in credit scoring, consumers’ average credit score tends to increase with age.

These are the average credit scores by age group in the United States:

- 20 - 29: 662

- 30 - 39: 673

- 40 - 49: 684

- 50 - 59: 706

- 60+: 749

How can I check my credit score?

Consumers can get a free copy of each bureau’s version of their credit report once per year. To request a copy of your credit report, you can fill out a request at http://www.annualcreditreport.com/ or call 1-877-322-8228. You can also request a copy by mail by sending a form to Annual Credit Report Request Service, P.O. Box 105281, Atlanta, GA 30348-5281.

How can I read and interpret my credit score?

Your credit score is just a number. It can offer a quick idea of your creditworthiness, but it doesn’t provide the whole picture. You can interpret your score using the score ranges that Experian, one of the major credit bureaus, offers these guidelines:

- Very poor: 350 - 579

- Fair: 580 - 669

- Good: 670 - 739

- Very good: 740 - 800

- Excellent: 800 - 850

To really understand your credit score, you’ll have to look at your credit report, which includes the details that determine your credit score. Your report contains all of your payment information, including on-time and missed payments, your different loans and lines of credit and balances of each, and all of the other information lenders look for when making a lending decision.

How to improve your credit score

Your payment history makes up the greatest portion of your credit score, so one of the best ways to increase your score is to make on-time payments and avoid late payments at all costs. If you do miss a payment, it will take time to restore your score to its previous standing.

Another important factor in building and maintaining good credit is minimizing the amount that you owe. Typically, the less money that you owe, the higher your credit score will be. Having accounts, like credit cards, open lets you build a payment history — But paying your bill in full each month will keep your balances low, which can help your score.

Applying for new credit lowers your score in multiple ways, making it important that you only apply for new credit cards or loans when you need them. First, applying for a card shows up on your credit report as a hard inquiry, which drops your score slightly. If you’re approved, the average age of your credit accounts will fall, causing another drop in your score.

Of course, having more old accounts will make the impact of a new account on your average age of credit smaller. This makes keeping older lines of credit and credit cards open (even if you don’t use them often), helpful for building credit. However, try not to pay annual fees if you don’t have to.

One thing you can do to improve your score is to check your credit report for errors. If a credit bureau has incorrect information on your report, you can request that they correct or remove it. If the incorrect information is harming your score, getting it removed can boost your credit. Each bureau has its own process for requesting a change to your report, but typically they require that you submit your request in writing.

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock. Securities trading is offered through Robinhood Financial LLC.