What is a 403b Plan?

A 403b plan is a retirement savings plan, much like a 401(k), for employees of public schools and other nonprofit organizations.

🤔 Understanding a 403b plan

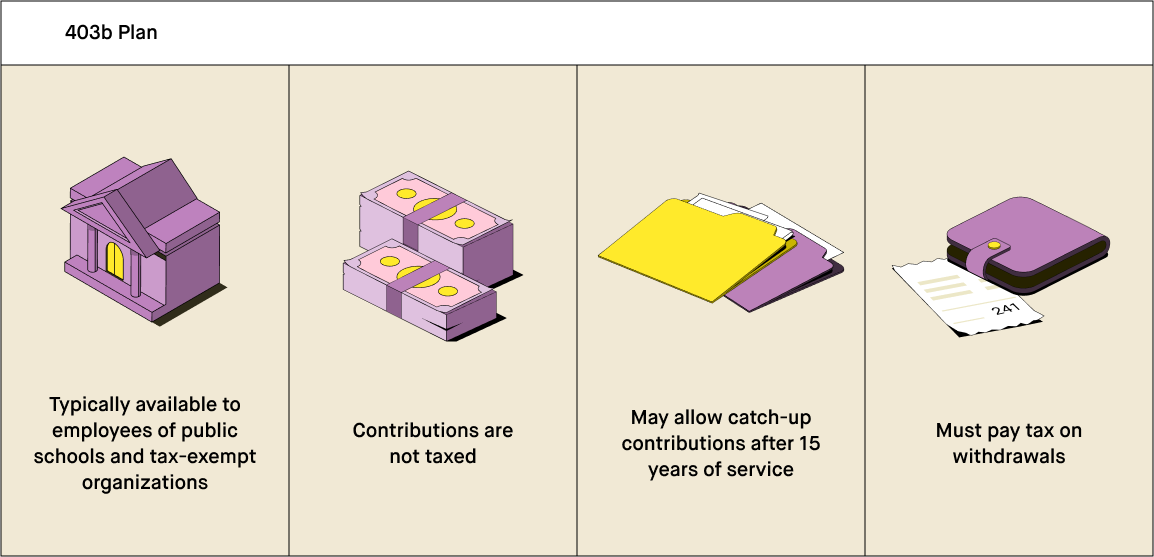

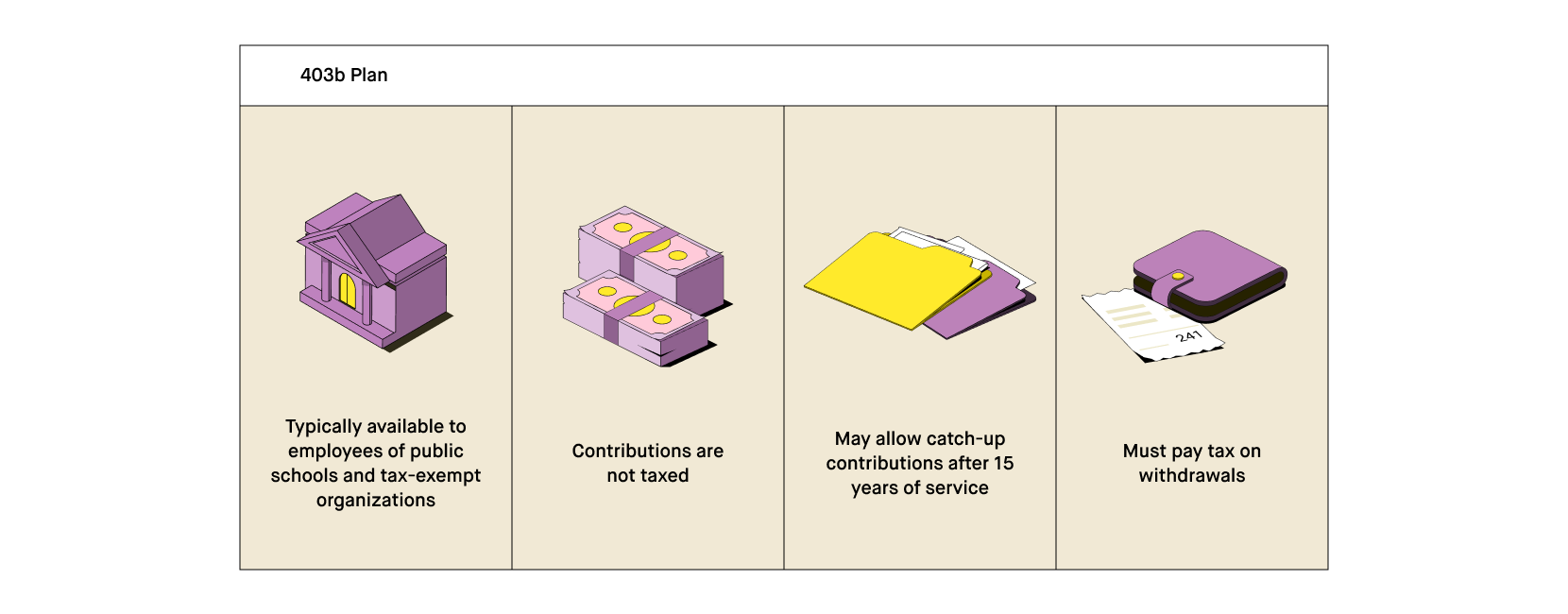

A 403b plan — also written as 403(b) or 403 b — is a retirement account for employees of many nonprofits and certain government employees. It resembles a 401(k) for private-sector employees, but has some different tax implications. Typical employees qualifying for 403b accounts include public school teachers, professors, government employees, nurses, and librarians. These plans allow you to contribute money on a tax-free basis, like a 401(k). Once you've signed up, your employer will deduct money out of your paycheck. In some cases, your employer may even match your contributions. These contributions are not taxed. Growth of the money in these accounts is tax deferred — You only pay taxes when you make withdrawals later in life. Some 403b accounts, unlike 401(k)s, allow for catch-up contributions of $3,000 a year once you’ve served for 15 years at certain institutions.

Imagine an economics professor who accepts a position at a state university. As part of her employee orientation, she receives information about the 403b plan. She fills out an application stating how much she would like deducted from her paycheck. Her employer matches some of her contributions. In 20 years, the professor has grown her 403b account tax-deferred and decides to retire. For the last five years, she’s been allowed to make extra catch-up contributions of $3,000 a year that would not have been allowed under a 401(k) in the private sector. She now has been able to save a bit more than she would have been able to in a private-sector 401(k), and she pays taxes when she withdraws money from the account.

Takeaway

A 403b is like a very large piggy bank specially designed for teachers and other government and nonprofit workers…

Similar to a piggy bank, a 403b plan allows you to put money away for later. Since government and nonprofit workers are assumed to have sacrificed some pay by working for lower-paying employers, the government throws in a few extra tax benefits.

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock. Securities trading is offered through Robinhood Financial LLC.

How does a 403b work?

A 403b plan is available for employees of public schools and tax-exempt organizations such as religious groups and charitable organizations. It is like a 401(k) plan, another retirement account sponsored by private companies. A 403b takes money out of an employee's paycheck and places it into a retirement account tax-deferred. The 403b helps employees plan for retirement. There are two types of investment options. The first is through an account invested in mutual funds. A mutual fund allows people to invest in a mix of stocks and other securities. The second is an annuity contract provided by an insurance company. An annuity is a financial product that an individual can purchase that provides fixed payments to the annuity holder.

Most 403b plans offer the investor the ability to borrow from their account. The rules vary with each plan, but many plans allow a loan in the case of an emergency. At most, an individual may borrow 50% of their current account balance or $50,000 — whichever is lower. In general, the loan must be paid back within five years and payments must be made at least four times a year.

Who can contribute to a 403b?

To be able to contribute to a 403b, you must work at a nonprofit, public school, or a church. You cannot set the plan up yourself — It must be set up by your employer. If you are eligible to make contributions to a 403b, you must be aware of the tax laws each year.

In 2023, if you are under 50 years of age, you can contribute up to $22,500 (up from $20,500 in 2022). If you are over 50 years of age, you can make another contribution. This contribution is called a catch-up contribution. It is a separate contribution for people over 50, allowing them to contribute $7,500 more each year (up from $6,500 in 2022).

There is a second provision that enables employees of any age to contribute an extra $3,000 per year. There are limits to this contribution, though. First, to qualify, you need to have completed at least 15 years of service with the same employer and your average annual contributions cannot exceed $5,000 per year. Second, there is a lifetime limit of $15,000 for this catch-up contribution.

You may even be lucky enough to work for an employer that matches your contributions. This is called an employer match. An employer may contribute the same amount that you contribute, up to a predetermined amount.

What are the 403b withdrawal rules?

You can start taking withdrawals from your 403b when you reach the age of 59½ . You are not required to take withdrawals at this age, though.

If you make withdrawals before 59½, you may need to pay a 10% early withdrawal tax. The 10% penalty is after the income tax you will pay on your withdrawals. After age 59½ , you will only pay income tax on the withdrawals.

Some situations allow you to make early withdrawals without a penalty. For instance, if you retire at the age of 55 or older, you can make withdrawals without penalty. If you leave a job, you can transfer your 403b account into an IRA. An IRA is another type of retirement account that allows your money to potentially grow tax-deferred. You need to set up this type of account yourself and select your investment options.

For a 403b, you need to start making withdrawals by April 1st of the year after you have turned 72 years old (70 ½ if you reached 70 ½ before January 1, 2020). There is one exception to this rule. If you are still working, you can postpone your withdrawals until the year after you have retired.

What are the advantages and disadvantages of a 403b?

As with any retirement plan, there are advantages and disadvantages to a 403b.

The most significant advantage is that money in a 403b can potentially grow tax-deferred until you withdraw it. If you are eligible for a 403b plan, you may also receive contributions from your employer. Think of this as free money. When employers deduct money from your paycheck for a 403b plan, your take home pay is reduced. The lower income can result in less income tax. You can also take loans against your 403b, as long as you pay the loans back.

A disadvantage of a 403b plan is the number of investment choices available. 403b plans have fewer investment options than an IRA or even a 401(k) plan. While some plans may offer specific mutual funds, many only provide an annuity. An annuity is a financial product offered through insurance companies. It can provide fixed payments to the annuity holder. Another disadvantage to a 403b is that in many cases, you can't make penalty-free withdrawals until age 59½.

What is the difference between a 403b and a 401(k) plan?

A 403b plan and a 401k plan are very similar types of retirement accounts. They both have the same contribution limits, in most cases. They also have the same withdrawal age of 59½, and both offer the $7,500 catch-up contribution for individuals who are age 50 or over. The main difference between 403b and 401(k) plans is that 401(k) plans are generally available to employees of private or public companies. A 403b plan is open only to employees of nonprofits and the government.

There are some other differences as well.

The first is the limited investment choices in a 403b. Mutual fund companies often administer 401(k) plans, while insurance companies usually administer many 403b plans. Mutual fund companies typically offer more investment choices for 401(k) account holders. Annuity products in 403b plans also charge fees generally not found in 401(k)s. Employers who sponsor 403b plans are also less likely to match contributions. Finally, 401(k)s do not offer the $3,000 catch-up contribution that may be available to eligible 403b account holders.

What is the difference between a 403b and an IRA?

A 403b plan and an IRA are two different types of retirement accounts. They both offer a way to potentially grow your money tax-deferred. An employer sponsors a 403b plan while an individual needs to open an IRA at a brokerage firm. A brokerage firm allows you to buy and sell securities like mutual funds and stocks.

Since an employer sponsors a 403b, they can make contributions to your account. An employer cannot make contributions to your IRA. You are the only one that can make contributions to your IRA account.

There are also different contribution limits. In 2023, you can contribute up to $22,500 in a 403b, but you can only contribute up to $6,500 in an IRA. You can contribute up to $7,500 in an IRA if you are older than 50.

There are more investment options in an IRA. You are free to invest in different types of mutual funds, stocks, and bonds. A 403b typically limits available investments to annuity contracts and a select list of mutual funds.

Robinhood does not provide tax advice. For specific questions, you should consult a tax professional.

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock. Securities trading is offered through Robinhood Financial LLC.